Corporate banks are seeing income squeezed in many areas but investing in

new transaction banking solutions offers the potential of increasing returns

The global slowdown and trade wars have taken their toll on the corporate banking business of international banks. Corporate banking is challenged by stagnant portfolios, higher provisions and the growing cost of risk and coverage, which has reduced both income and profitability.

It is imperative that banks move to digitise their corporate banking transaction volumes in order to reduce the cost per transaction and improve the accuracy and speed of their corporate banking services as a differentiator. Corporates are also matured with higher digitisation levels and increasing pressure on reducing their own transaction workforce in order to drive value added activities in the workforce.

Cash management services such as liquidity management, collections & receivables & payments are expected to contribute a 65-70% of global transaction banking (GTB) market revenues followed by trade finance and supply chain. These revenues are likely to increase this year to $1406 billion at a compound annual growth rate (CAGR) of ~7% as per recent research. Customer demand for trade finance, supply chain & treasury is yet to pick up on digital platforms

Trend 1: Build a Best in Class Transaction Banking Platform with the Right Model

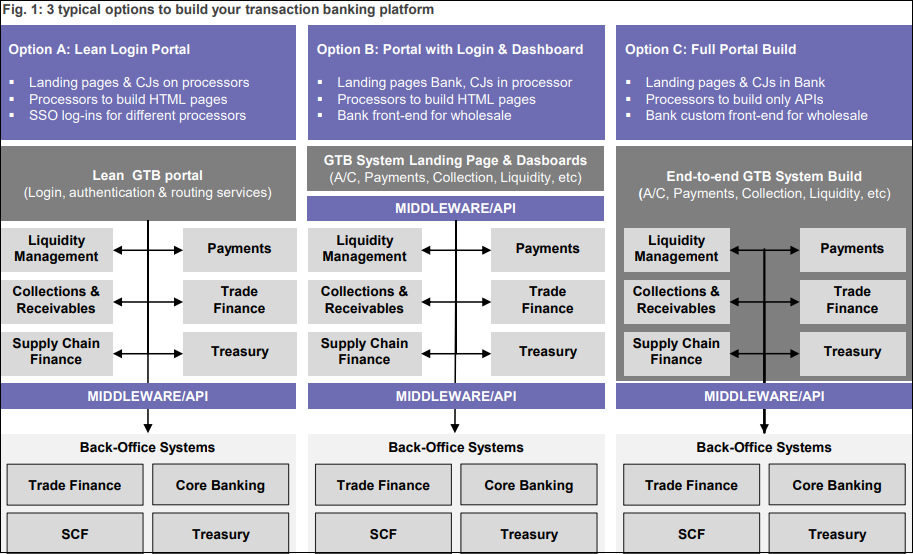

There are three typical options available to banks looking to build a GTB platform. See Fig. 1: 3 typical OPTIONs to Build your Transaction Banking platform.

- Build a Lean Portal (Login, Authentication Services): In this model post-authentication the portal is wired to front-to-back product processors (for Payments, Collection, Trade Finance and Supply Chain) to ensure complete coverage of the functionality and straight through processing. The model comes with advantages such as lowest time to build (6-9 months) and fastest build revenue. However, the model lacks the ability to put in a landing page with a multi-product analytics page and requires individual product processor landing pages through multiple clicks and logins. Many young and single back-end platform banks prefer this model.

- Build a GTB Portal with Persona based landing page with analytical dashboards for Cash (Account Services & Payments, Collections), Trade Finance and Supply Chain product lines. This model comes with advantages such as differentiated customer experience based on product persona, the best of both worlds in terms of back-end product processor leveraged and front-end portal delivering its unique experience. This model comes with disadvantages such as higher build cost, longer build time (12-15 months) but offers the availability of product APIs for dashboards and analysis. Many leading banks use this approach, such as First Abu Dhabi Bank, Emirates NBD, Qatar National Bank, HDFC and Kotak Bank to name but a few.

- Build a GTB Platform with Comprehensive end to end functionality for Cash (Account Services & Payments, Collections), Trade Finance and Supply Chain product lines. This model comes with the advantage of complete differential and custom experience based on personas. A complete customer journey is designed, built and delivered through a custom developed portal resulting in the financial or non-financial transactions managed and maintained in the portal and handed off to the back end through an API for financial posting and reporting. This model comes with the disadvantages of the longest time to market, longest timeframe for development (18-36 months) and the need for significant knowledge of GTB platforms which is must. Most very large international banks use this approach, including the likes of HSBC, Standard Chartered Bank and Citi.

There are multiple solutions available in the transaction banking space from vendors such as Intellect Design Arena, Finastra, Backbase and innovative challenger players such as Mindgate, CashFac, NeuroSoft among many others.

Trend 2: Design Intuitive Customer Journeys & Experience Based on Personas

Corporate banks should gather deeper insights into how customers are using their solutions and continuously improve these solutions with help of experience design through customer journey (CJ).

CJ is a tool to draw the customer journey in terms of click, inputs and bottlenecks as well as the overall journey. Global transaction banks are increasingly focusing on customer experience in order to simplify their portals and driver higher digital adoption among corporate personas.

A persona is defined as a corporate banking user role doing a specific function such as Treasurer, CFO, Payments Maker, Payments Checker, Collection Maker, Trade Finance Verifier and etc. Persona-based experience design is seen as a major investment in 2020-21 by GTBs with significant budget allocated to drive adoption in this area.

Personalisation allows business users and end customers to customise the solution interface and experience to their own expectations. For GTB, put at ~15% of corporate banking income has become significantly more relevant in business terms example, one of the leading global wholesale banks invested $2 billion in 2019-20 In modernising its transaction banking platform through an in-depth study of its customer experience delivery.

Trend 3: Build a SMART Client Onboarding Solution by Segment

As channel adoption is increasing among corporates it is becoming important to build a SMART end-to-end omni-channel solution to facilitate onboarding of new to bank (NTB) customers from self-service and assisted channels for NTB and existing to bank (ETB) clients.

Recent research shows seven out of 10 corporate banks are likely to invest into their onboarding solution for specific corporate segments such as SME, MSME and large corporates. The trend also depends on the level of sophistication of the marketplace. Digital authentication for corporate signatories may not be easily available. In the UK Tide Bank, targeting an SME customer base has designed an innovative onboarding solution.

However, the pre-requisite for such a solution requires a directors’ registry and the availability of an authentication mechanism. Several banks around the world are investing in onboarding solutions with the ability to validate identity manually until a digital authentication library becomes available.

There are multiple suppliers available in the onboarding space such as i-exceed Solutions, Backbase and many tier-1 software developers are doing very interesting work in this arena.

Trend 4: Modernise the Architecture with Microservice & Apps.

GTBs are now modernising their technical architecture for providing Omni Channel Experience. This requires the bank to provide a consistent experience across mobile and web channels using a single solution rather than distinct channel specific solutions. This is enabled using micro services and apps architecture.

Banks need to design solutions based on micro apps and micro services instead of monolithic structures to facilitate easier and faster plug-and-play of specific features. Given the availability of the FinTech eco system of suppliers for specific activities, the micro services architecture becomes even more critical.

With corporate customers consuming these new micro services to perform specific functions, this allows GTBs to look to generate new sources of income around API-based pricing on volume and services consumed. These investments could be self-funded due to independent revenue streams from the partner to the banks. Testing these micro services and applications is done using RPA Test Automation. This minimises development and delivery timelines.

Trend 5: Self Service is the Best Service

As already mentioned, one leading bank invested $2 billion n modernising its transaction bank platform through an in-depth study of its customer experience delivery and improving the “administration” module. Typically, a transaction bank supports “bank administration” which means the bank administers the users and entitlements, adding new users and enabling the different products and transaction types. However, banks have been increasingly moving towards “shared administration” which means the corporate customer will have administration rights to create its users and entitlements which are approved in some cases by the bank administrators

The next generation of transaction banks’ development will create “self-administration”, which will mean that administration roles inside the banks will tend to disappear for SME and low price segments and the bank will provide corporates with full capability to do its own administration of users, entitlements and the products and services it may avail. Self-administration will allow the corporate to onboard the company across multiple products and create its own users, groups, linked limit structures and set transaction limits and processing rules. It will also allow corporates to personalize the workflow, dashboards and analytics for each persona.

Self-services is likely to reduce the costs of transaction banks by 25- 30% as manual back office operational roles will disappear. However, this will also require corporate to have enterprise fraud engines to detect fraud patterns in case of cyber-attacks.

To read more such insights from our leaders, subscribe to Cedar FinTech Monthly View