The next phase of growth in Islamic banking will be driven not just with the offerings

that are compliant of Shariah and its positioning vis-à-vis conventional banking,

but will have to be on the basis of differentiation, driven by innovation

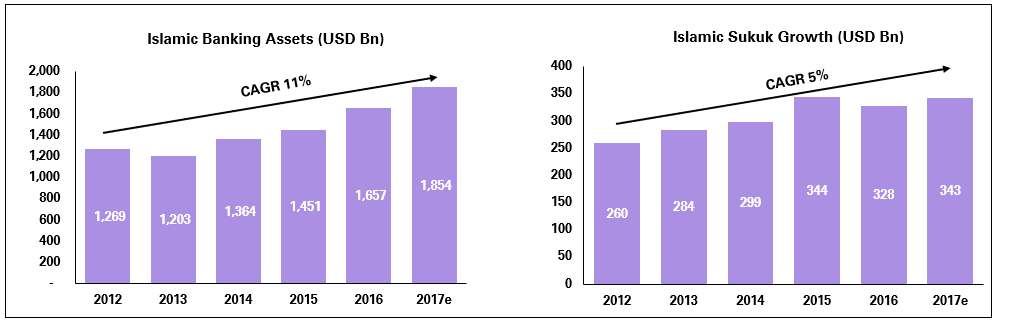

That there has been a remarkable 11% growth in global Islamic banking assets over the last 5 years , compared with 7% growth for conventional banking assets. This is not to be brushed aside as a one-off phenomenon, for the simple reason that this growth is not just limited to the Middle East or Malaysia, but has been increasingly prominent in Africa, Central Asia and also the Far East. Interestingly, Islamic deposits have also seen a 7% growth over the last 5 years, while Sukuks – the Islamic bonds – have been steadily on a growth rate of 5% too.

There are three significant things one could attribute this growth to:

The increasing customer demands, that have been fairly consistent and evident in the growth that have been witnessed both in the corporate and retail banking segments.

The opening up of a regulated Islamic banking market – especially in the Middle East, North Africa and many parts of Asia has allowed for banks to serve an untapped segment.

More importantly, banks have found the benefits of having an Islamic window that compliments the conventional offering, both from a customer segment and a product portfolio standpoint.

Islamic banking has been growing steadily over the last 5 years

Interestingly, the advent of Islamic banking drove innovation through a new set products and services that were Shari’ah compliant. However, as the segment has grown, and continues to grow, the need for differentiation, primarily driven through innovation has become inevitable focused more on differentiated customer segmentation, product bundling and positioning, and driving innovation through technology. Let us explore these three areas of innovation a little further.

"One of the key tenets

of any successful Islamic

bank is in the successful

segmentation of its current

and potential customer base"

Segment based offering

One of the key tenets of any successful Islamic bank is in the successful segmentation of its current and potential customer base. For starters, the misconception that Islamic banks are primarily for the Muslim population can limit the potential of any bank, deeply. The corollary to that is also important: a large segment of customers subscribe to the bank’s services more to receive the offerings that cater to its needs, than for purely religious reasons.

Developing a distinctive customer segment – not just based on the income levels and the classic segmentation of mass retail, affluent and HNI, but also based on the demographics – such as Islamic banks looking to drive innovation through synergistic partnership age group, focus groups, etc is critical. Driving innovation in the product positioning and partnerships is a function of having this defined well.

Product bundling

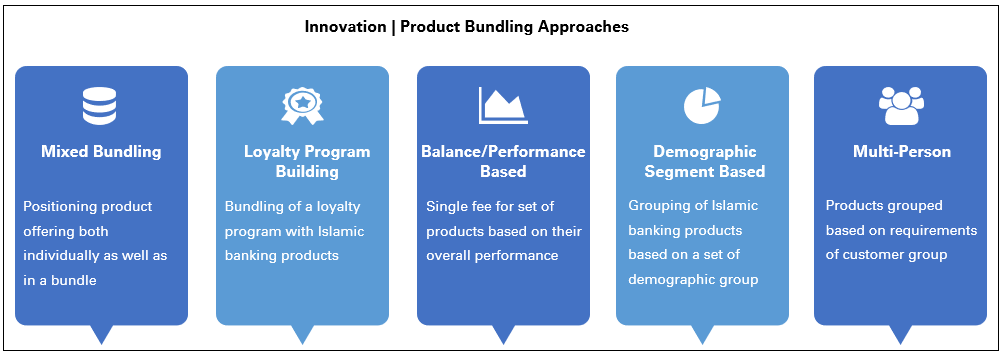

As is evident from the experiences of Islamic banks across multiple countries, the key to driving innovation in products in the next phase of growth is in the efficacy of the bundling strategy. There are essentially 5 types of bundles that banks are looking to drive:

Mixed bundling: where the existing individual products get to be offered as a bundle. This is quite typical of any banking offering, where Islamic credit cards, for example, get bundled together with an asset product.

Loyalty bundling: this gets more interesting, as Islamic banking products get bundled with Shari’ah compliant loyalty programs. There is a fair degree of financial estimation and innovation in fee structure that may be critical here. Additionally, many of the earn/ burn partnerships may have to carefully reviewed, to align with Shari’ah principles.

Balance based bundling: driving effective cross-sell, with a singular fee model across products. This is particularly useful in the Islamic banking context, where there are fees designed for most products, and building an integrated balanced based bundling approach can be quite convenient to the customer and also effectively drive cross-selling.

Demographic bundling: aligned with the segmentation discussion we had earlier, driving a bundling program around demographics such as gender, age, profession, and location. This can particularly be useful where an existing conventional bank is looking to drive its Islamic window, and prior understanding of the existing customer base can help drive demographic penetrations.

Multi-people bundle: Driving a larger bundle for a group – typically a family, to provide efficacy of multiple offerings. Considered an extremely effective product innovation in the Islamic context, this helps in broadening the offering, particularly in the retail context.

If one looks at the bundling elements carefully, it would be no surprise to note that many of these have also been adopted by conventional banks. However, the key differentiator here is the fact that both the bundle, and also the innovation in the structure of the offering, need to be cleared by the Shari’ah board, which regulates the new product offering and validates its compliance to the Islamic banking principles. One needs to note that the method in arriving at the fee structure is derived from the profit pool calculations, and is not as straight forward as in the conventional context. The other important aspect here is the fact that one could potentially align with the value principles promoted by the Islamic context (eg. Product offering for all family members) to drive innovation in bundling of the products and its market positioning.

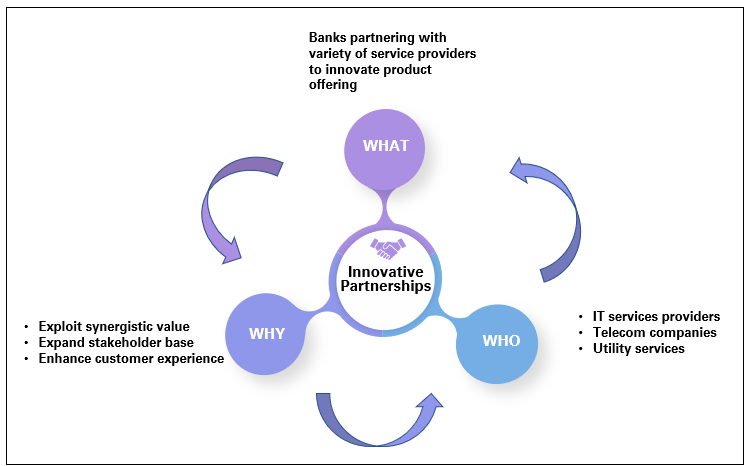

Just as product bundling is seen as a core innovation area, a natural corollary to this is the set of partnerships that Islamic Banks tend to build that help in driving synergistic value as a branch positioning, and also enhance the overall customer experience. Considering that there are restrictions that are

typically applicable in the kind of earn/burn relationships that can partnered with in the Islamic banking context, driving the right partnership and in the process enhancing the stakeholder value has a significant connotation to it. The most common partnerships are typically with utility service providers, travel partners and telecom service providers.

The single most important driver for most innovation across banks – both conventional and Islamic alike, cutting across geographies, can be attributed to the adoption of technology

Innovations in Technology

The single most important driver for most innovation across banks – both conventional and Islamic alike, cutting across geographies, can be attributed to the adoption of technology. Adapting to new age cool-fintech trends of cloud, digital, big-data and analytics is but a given. The nuances of co-existing conventional and Islamic banking platforms can be daunting for a conventional bank looking to also build an Islamic window, especially if you have not thought through the experience from a customer’s angle.

For starters, and as we discussed earlier, if one parks the customer segment that is using the service purely for religious reasons aside for a moment, the rest of the customer base is quite indifferent to the Shari’ah angle, but more sensitive to the overall experience and the value proposition offered. So much so, that the same customer could be using a set of products with the conventional bank, and also subscribing to a set of additional services through the Islamic window, with the expectation of having a consistent experience across both. While the innovation and focus in the customer segmentation, product positioning and partnerships can help with the value proposition, the piece that can make a significant impact is the technology-driven innovation.

While there are several aspects to technology innovation, the piece that is of utmost relevance from a conventional-Islamic banking co-existence standpoint is driving the right omni-channel experience for the customer. In simple terms, the customer is keen to experience banking on a consistent basis, quite independent of which channel he or she is engaged with – be it the branch, the ATM, the internet or the mobile channel, and also not requiring to identify oneself separately for being the customer of the conventional and Islamic bank respectively. Taking this one step further, omnichannel experience is also about driving the execution of a transaction across channels. Consider this: If a customer could request product details on the internet, make the subscription on the mobile, activate the service over a branch, visit and check the balance over the IVR, all in the same breadth, then chances are that the technology integration is well done!

From an internal application architecture standpoint, the conventional and Islamic core banking systems need to coexist and talk to the aligned applications – be it the credit card management system, retail lending systems, risk management applications, workflow and process management systems, back office applications for treasury and trade finance, or for that matter integrating with the centralized supports systems including GL.

While this is indeed an option for banks that have established solutions in both conventional and Islamic space – such as Finastra, FIS, Infosys, Oracle, TCS, Temenos – one also comes across several banks that have opted the specialized Islamic offering from the likes of BML, ICSFS, ITS, and Path solutions as a complimentary solution to their existing conventional platform. The historic approach of building connectors across all the applications is passé. While most banks that have an Islamic window tend to connect using the middleware, there are also large banks that prefer retaining the existing conventional platform provider, to also extend the Islamic offering.

Way forward

Any innovation that does not pass the litmus test of driving customer experience is not worth its investment. And therein lies the secret sauce. While most innovations that have been adopted in the last decade have been focused more on the product and technology, one would expect that the disruption that is being experienced elsewhere in the larger banking context will have its own Islamic flavours in the not so distant future. This could only mean two things:

One would expect that the disruption that is being experienced elsewhere in the larger banking context will have its own Islamic flavours in the not so distant future

Keeping with the times, in terms of customer expectations is key. Driving innovations to be aligned with this focus is a pre-requisite for success, in addition to the compliance of norms.

Understanding the essence of innovation driven in the conventional banking context – across customer experience, channels, process innovation, product design and technology solutions – and adapting them from an Islamic context will be critical.

It is not rocket-science then, that both the above emphasize and zero-in back to the same point. At the end of the day, Customer is King!

To read more such insights from our leaders, subscribe to Cedar FinTech Monthly View