For most banks the answer to this simple question is “no”!

I reach this conclusion not from a sophisticated evaluation of questions such as: “Is the bank using state-of-the-art customer relationship management and database segmentation techniques?” or “Has the bank optimized the application of Chip and Pin (EMV) technology at point of sale?” Instead, I have observed that in today's fast-paced credit card industry many banks have forgotten the “Don't run until you can walk” principle. Put another way, “when you move away from the basics….don't forget the basics”

Whilst it is tempting to use “best practice” examples to illustrate these messages (and indeed benchmarking to “best practice” can be an essential management tool), sometimes we can learn more from a “poor implementation” than from best practice itself. For example, in situations where a best practice established in one market is not appropriate for a different market situation. Or, from one bank to another bank that has a different structure, processing platform or competitive environment.

I began my career over 20 years ago, working in credit card businesses in the UK and European markets. At that time, they were still in the early “development” phases for payment systems and per capita holdings of credit cards were a fraction of what they are today. Many banks jumped on the bandwagon (of) offering credit cards without truly understanding how to get the most from the product and its contribution potential in terms of “customer retention”, “new customer acquisition” and “profitability”. Some of these banks have since progressed to become highly sophisticated product and brand marketers, yet even today remarkably few still receive high marks across the board.

To illustrate this, I highlight some observations from my visits in the past two years to the European card operations for two top ten global banks

- The first bank was, for more than a decade constrained from enhancing its core credit card product offering, and was unable to deliver targeted benefits to different customers. This was due to its reliance on a shared processing capability with a centralized processor that also provided equivalent services for several of its largest competitors. Even with the largest retail bank network in the market and leading brand position, the bank had steadily lost market share to more nimble competitors and new entrants, because of its inability to provide any meaningful differentiation in its products.

- The second bank had, over a period of two decades, added so many new products that it was unable to effectively distinguish.which communications and offers were relevant to which product holder. The bank had focussed only on the approximately 58% holders of a handful of relatively recent products and virtually ignored the other 42% (including some of the banks long-standing and high value customers who were never migrated from older products as these generally carried higher interest rates). The result was a confusing mix of more than 40 products which created an impossible challenge for its extensive product management team to coordinate. It also delivered negative relationship differentiation to many of the top customer segment

During the past decade my work has been increasingly focused on developing markets, particularly in Eastern Europe and Latin America. In these markets there is, of course, an exceptional pace of development, together with growing market competitiveness. However, I also see many parallels with my experiences in Europe many years ago and even with smaller financial institutions in the US. Many banks in developing markets are focussing on some important aspects but showing a lack of balance in other core business areas. By not “getting the basics right” across the board, they are setting themselves up for disappointment and under-performance. I know of many instances where banks have made significant investments to pursue best-in-class solutions (e.g. with international processing, CRM or loyalty platforms), but then failed to deploy them in a balanced and effective way.

Some developing market examples:

- An Eastern European bank made a significant investment in a co-branded credit card with the country's leading mobile phone operator (market share of over 40%). The marketing materials were well developed, the card looked great but the launch was a complete flop. How could this be? Well, for years the bank had been underperforming with its own credit card offering. Instead of looking inwards and improving the viability and appeal of this product (features, pricing and accessibility), it expected to leapfrog to success by a co-brand partnership that would reach a whole new audience. Unfortunately, in launching the new card, the partners did little more than add a logo, change the look of the plastic and start an expensive advertising campaign. The core product flaws were not addressed and no added value to the phone customer was included (no loyalty program, no discount on off-peak hours, no SMS balance check). Basically the product had little relevance and very limited appeal!

- Another bank decided to re-focus its credit card product line to appeal to a more youthful “young urban professional” audience. They did some things right; invested in research, hired an excellent advertising agency and developed a 'hip' new design and brand name. However, they were so focussed on the image that they failed to deliver a solid product and service offering. The product also had no substantive features to appeal to the youthful audience that they were trying to reach. They did not match competitor offerings for either price or convenience. Risk criteria were imbalanced with: high negative scores for 'time in job below 3 years' (that typically this segment experienced) and also 'mobile phone only' (even though new landlines had a wait of over 12 months and were increasingly not pursued by younger professionals). All of this was compounded by focusing the bulk of launch investment in broad based rather than targeted initiatives. Not surprisingly, low response levels and approval rates resulted in a very poor performance and wasted investment.

- An international bank group had spent a huge amount of time and effort consolidating the credit card businesses of its six acquired regional banks onto a shared technology platform using a centralised group processor. However, two years later, the banks were still developing, launching and trying to refine their credit card businesses independently. The reason they had failed to optimize their technology investment was a simple one. The technology migration had been treated purely as an IT department objective (based on future ability to drive economies of scale). They had not looked at the technology in the wider context of group or market strategy or effective business coordination. In particular, they did not have any consistent 'country' or 'group' level perspective on business performance (beyond 'total cards' issued and 'total spend' in period), and each of the banks simply proceeded in a variety of 'hit and miss' initiatives and overall weak performance. If just a proportion of the effort taken in the systems migration had been allocated to the bigger picture of how to manage and track the credit card businesses, the banks individually and collectively would have been dramatically more successful.

So what are the “basics” for a healthy credit card business?

1. Organizational Awareness and Support

Credit cards can make a major contribution to a retail bank. When well developed and marketed, they can augment both the depth and loyalty of relationships with existing customers. They can also serve as a magnet product to attract new clients to the franchise. Credit cards can also be highly profitable - according to European market analysis from Datamonitor, they are approximately 10 times more profitable than debit cards and two and a half times more profitable than charge cards.

The most common failings here are:

- Insufficient strategic support and prioritization versus other lending products

- Inadequate organizational linkages between key functions (notably card operations, technology, marketing, finance, call centre and risk management)

- Lack of adequate business ownership (via direct or indirect reporting structures) and the disaggregating of P&L responsibilities

2. Sales effectiveness

Most banks do a reasonable job of reaching customers in the lowest risk band (by cross-selling), that part is easy. The key to success though is being able to reach creditworthy (more profitable customers) outside this initial base. As can only be achieved by developing compelling propositions to a broad segment of the bank's own customer base and also to attract and reach non-bank customers.

The most common failings here are:

- Imbalance in 'risk and reward' decisioning (usually due to lack of balance between Risk and Marketing function).

- Ineffective sales channels. For example: - Some customers (in developing markets, many customers) are still best reached at the branch. But often branches are not adequately equipped to sell and support credit card activities - Other customers want the convenience of 'online' or 'a person to talk to'. These functions are not difficult to establish but many banks do not have them

- Lack of sales incentive salesperson/channel reason to sell

- Lack of acquisition incentive customer reason to buy

3. Product Relevance and Appeal

For a product which has retained its core shape and functionality for over 50 years, the development of credit card offerings should be second nature to most banks. However, a remarkably high proportion of cards launched in all but a handful of markets (Notably US, Japan and UK) are simply 'me too' products. Today it is easy for banks to get into the credit card business and start issuing 'plastic' using functionality provided by a card scheme (Visa, MasterCard, Amex). What many banks often miss is the need to provide a compelling value proposition for customers to own and use their credit card.

The most common failings here are:

- The product offering is too bland to be appealing or too sophisticated for customers to understand.

- Product is embedded with expensive features that only a small proportion of prospective customers will value.

- Product is undifferentiated - doesn't do anything different, as well or better than competitor offerings. (e.g.: weak brand positioning, poor price value proposition, lack of loyalty component)

- Product is not relevant to client base (e.g.: high end customers, low end product)

- Product not relevant to lifestyle (e.g.: lots of great travel features but no value to non-travellers, or no online capability for customers who want to manage their financial relationships there)

4. Effective Risk management

Credit risk management is not the same as minimizing risk! It is the process of allowing issuers to make the effective lending decisions: Who to accept? How much to lend? What rate to offer? While it is easy to maintain low risk by having restrictive targeting and approval requirements, the art of risk management is finding the right trade off between risk and reward. This requires an understanding of customer risk profiles and the analytical tools to determine propensity to spend, revolve and default.

The most common failings here are:

- Lack of analytical tools or organizational expertise in risk management(including credit scoring, underwriting and scorecard development and refinement)

- Disconnect between marketing and risk functions in ensuring a balanced approach to customer targeting, approval processes, channel development and receivables management

- Failure to effectively use more advanced techniques such as introductory rates, balance transfers and systematic credit line increases.

- Lack of effective KPIs (key performance indicators) for risk function

- Absence of predictive modelling to identify 'at-risk' customers

5. Customer Lifecycle Communication

In these days of advanced CRM techniques, there is no shortage of expertise and technology that can help banks move towards best practise in customer relationship development. However, a remarkably common failing that I have observed is that banks fail to place anything like the same emphasis in communicating with customers after card issuance as compared to the effort and resources they place in attracting them to their product in the first place. Many mistake customer loyalty as something that can be achieved by a ‘magic pill’ of a rewards program. More fundamentally it is by effective and continued communication that banks can truly generate loyalty to their credit card programs.

The most common failings here are:

- Absence of effective welcome communications, including: reinforcement of features and benefits, first usage incentives, or service hotlines.

- Limited or no 'early months on books' communications (this is the key phase for stimulating spending and development of cardholder relationship)

- Lack of database analytics in developing increasingly “profitable” customer relationships (e.g.: spend incentives, credit line increases, loyalty recognition and risk communications)

- Poor attention to key segments e.g.: high potential customers, revolvers, reducing pattern spenders, likely non-renewals

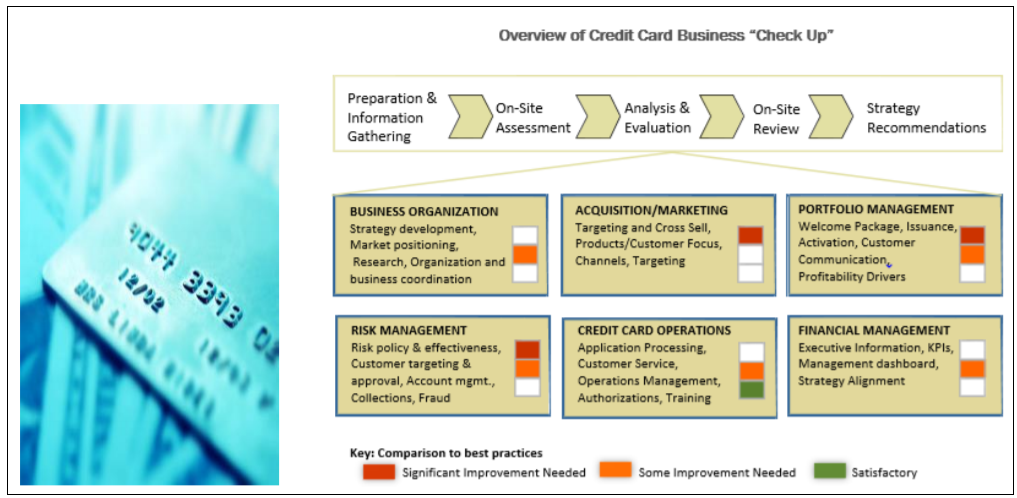

As I stated in the opening paragraph, banks will be well served by ensuring that they manage the evolution of their credit card businesses with a strong focus on the “basics”, and use that as a solid platform to adapt best practise and where possible to innovate. If your bank is not there yet, maybe it's time for a credit card business “check up”!

To read more such insights from our leaders, subscribe to Cedar FinTech Monthly View