Across the Middle East, business leaders are navigating one of the more complex operating environments in recent times. The companies that emerge stronger will be those that do not wait for the skies to clear – they will be those that chose to steer.

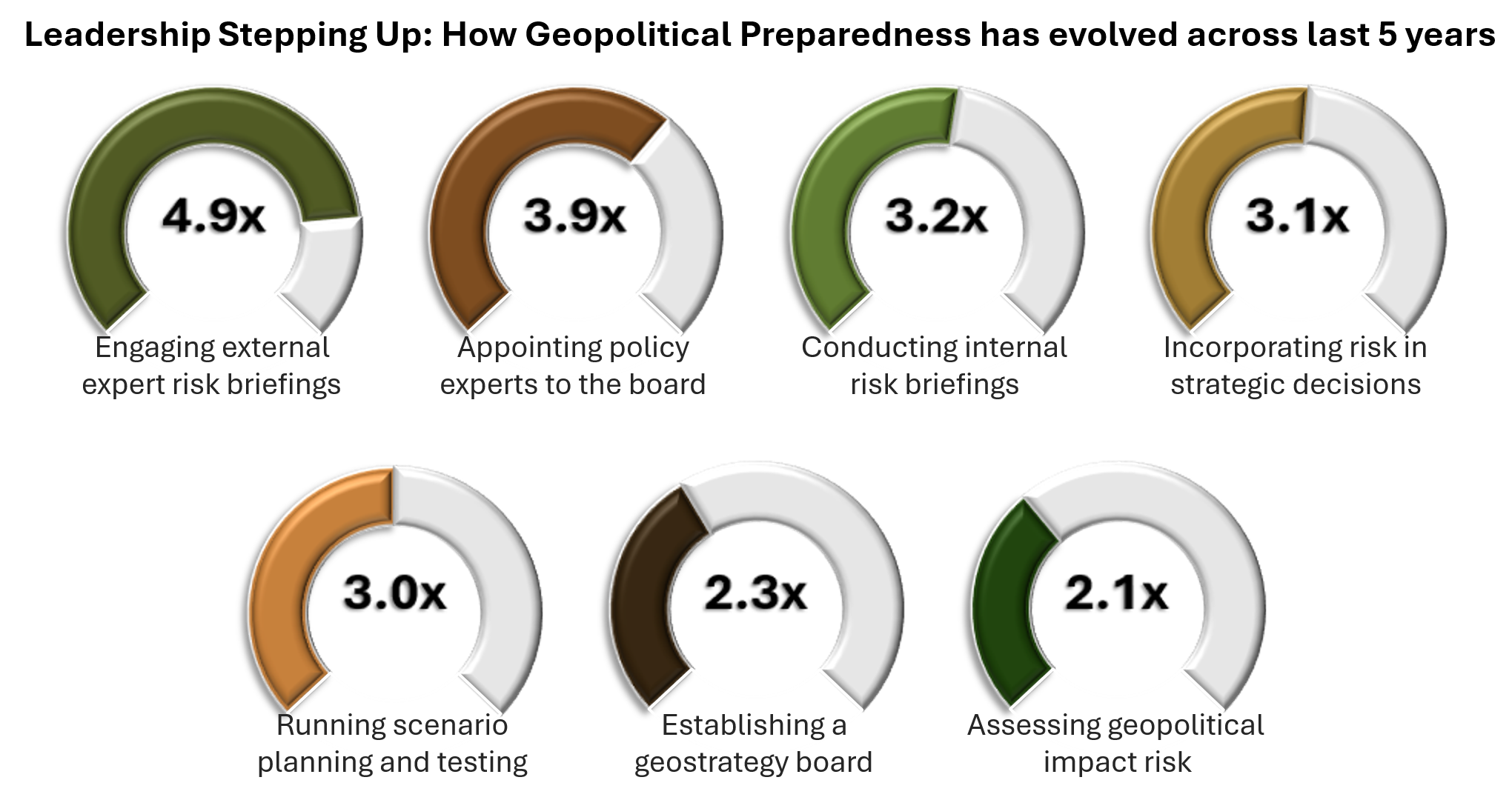

The scale of the current shift is worth noting. Boards worldwide are managing geopolitical risk across strategic dimensions at nearly 3.2 times the intensity over past 5 years- a clear signal that navigating complexity has become a core leadership discipline.

Data source: Cedar Research

Data source: Cedar Research

In the Middle East, the context is equally significant - the Strait of Hormuz carries 20% of the world’s daily oil and LNG flows, tourism spending across the region averages USD 600 million a day and working capital cycles for businesses across key sectors have stretched from 30 days to 60–90 days.

THE PAST AS A COMPASS

Data source: Trade Economics

Data source: Trade Economics

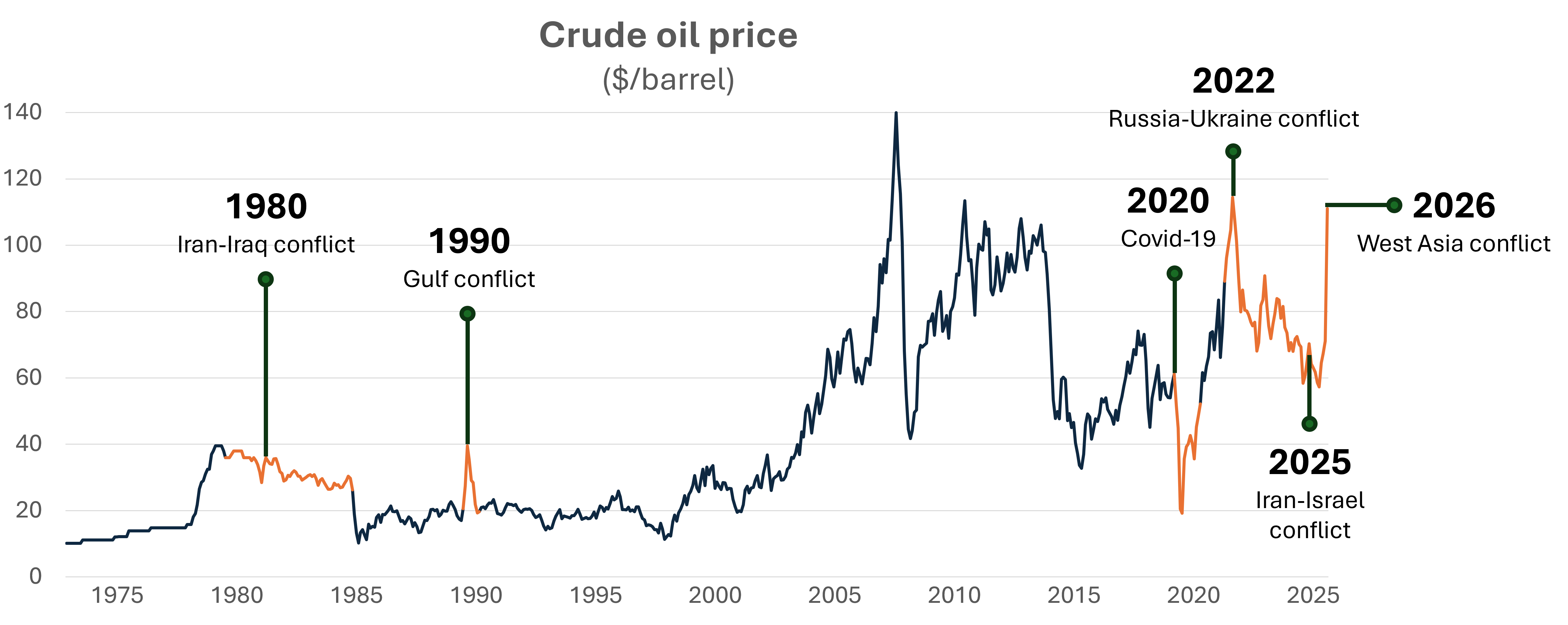

The past is not a perfect mirror but it is the most reliable guide available. To chart the path forward, it is worth examining how comparable periods of uncertainty had evolved.

The 1990 Gulf Conflict remains the most instructive reference point for the region. Oil prices surged 89%, private sector deposits fell sharply and trade routes that businesses had relied upon for decades were tested for resilience overnight. Supply chains for essential goods - food, pharmaceuticals, construction materials - faced sustained pressure and working capital cycles stretched beyond normal operating parameters. The businesses that had maintained operational discipline, protected liquidity and stayed close to their customers were the ones that emerged ahead of the field.

COVID-19 brought an entirely different dimension of disruption - one defined not by conflict but by the restriction of movement. Supply chains experienced unprecedented synchronization challenges, workforces were grounded, borders closed and the ability to deliver goods and services was constrained in ways no business continuity plan had fully anticipated. And yet the recovery was faster than most had expected. Companies that had protected their people, maintained customer relationships and preserved financial flexibility were the first to move - and the first to grow.

The Russia–Ukraine conflict of 2022 delivered a different but equally useful lesson. Commodity markets repriced with speed - European natural gas surged, freight costs escalated and global supply chains that had been optimised for efficiency were suddenly less resilient than expected. Businesses with diversified supplier bases and strong balance sheets navigated the period with measurably greater confidence. The conflict accelerated a structural shift in global trade alliances and energy flows - changes that outlasted the immediate disruption and possibly altered the competitive landscape for businesses across multiple sectors.

WHAT’S SHIFTING RIGHT NOW – INDUSTRY IMPACT ACROSS SECTORS

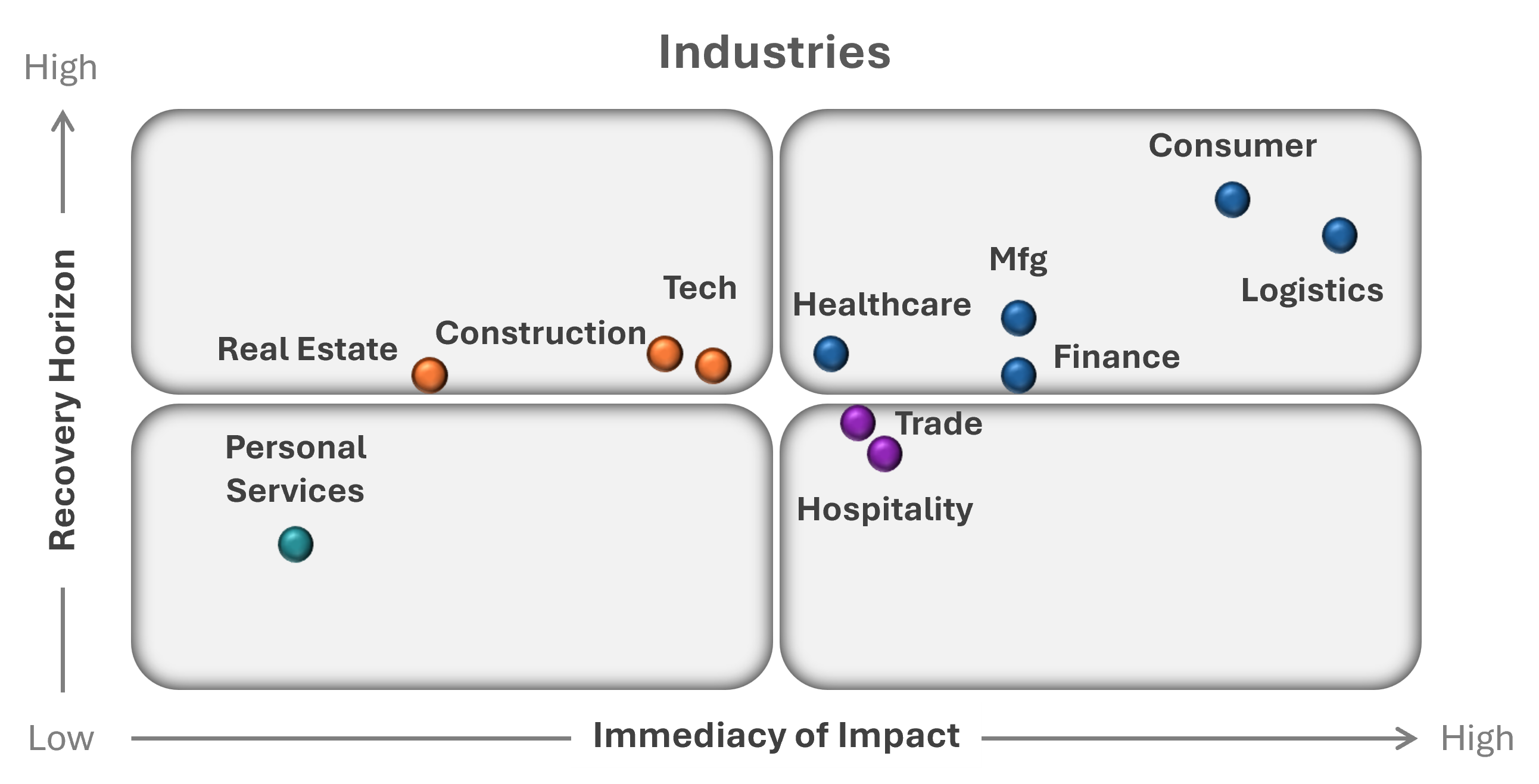

Every industry is feeling the pressure of the current environment - each at its own pace and path to normalisation. For leadership teams, understanding that position & planning accordingly is where strategic clarity creates competitive advantage.

Data source: Cedar Research

Data source: Cedar Research

- Logistics (Trading & Distribution) – With Strait of Hormuz traffic at near standstill, freight costs have surged and conflict-risk insurance premiums have reset structurally upward. Rerouting via the Cape of Good Hope is adding 30–45 days to trade cycles, stretching working capital and compressing margins across the supply chain.

- Consumer (Food & FMCG) – With the majority of Gulf states dependent on food imports, supply chain disruptions are translating directly into shelfprice pressure. Input availability is tightening, elevating food security to a strategic priority for both businesses and governments.

- Manufacturing (Energy & Industrials) – The commodity reset extends well beyond oil. Aluminium shipments have halted, with Gulf smelters producing metal they cannot move. LNG presents a more complex challenge – a single concentrated production complex in the region, restart timelines are measured in weeks, not days.

- Finance (Financial Services & Capital Markets) – Working capital cycles for SME clients have stretched from 30 days to 60–90 days, wholesale funding spreads are widening and investor appetite is moderating – all of which are manageable with early and deliberate treasury action.

- Healthcare (Pharma & Agriculture) – API and pharmaceutical supply chains are under logistics pressure, with airfreight disruption compounding sea route delays across several sourcing corridors.

- Trade (Retail & Luxury) – Air cargo disruptions have stranded garment shipments across South Asia, while discretionary spending is contracting as household confidence adjusts to rising input costs. Luxury segments face additional pressure from a demand environment already in transition.

- Hospitality (Aviation & Tourism) – Visitor spending across the region averages USD 600 million a day and forward bookings declined sharply as as air travel corridors were temporarily disrupted. Recovery in this sector has historically been swift when supported by clear government communication and traveller confidence.

- Technology (IT & Digital Infrastructure) – Helium supply – critical for semiconductor production with no viable substitute – is under strain and data centre operators are carefully weighing service continuity obligations against the realities of a disrupted operating environment.

- Construction (Real Estate) – Foreign demand is softening and new project launches are being deferred. Material supply delays are extending construction timelines and developers are adopting a measured approach to new commitments while the broader environment stabilises.

KEY DIMENSIONS EVERY LEADERSHIP TEAM MUST NAVIGATE

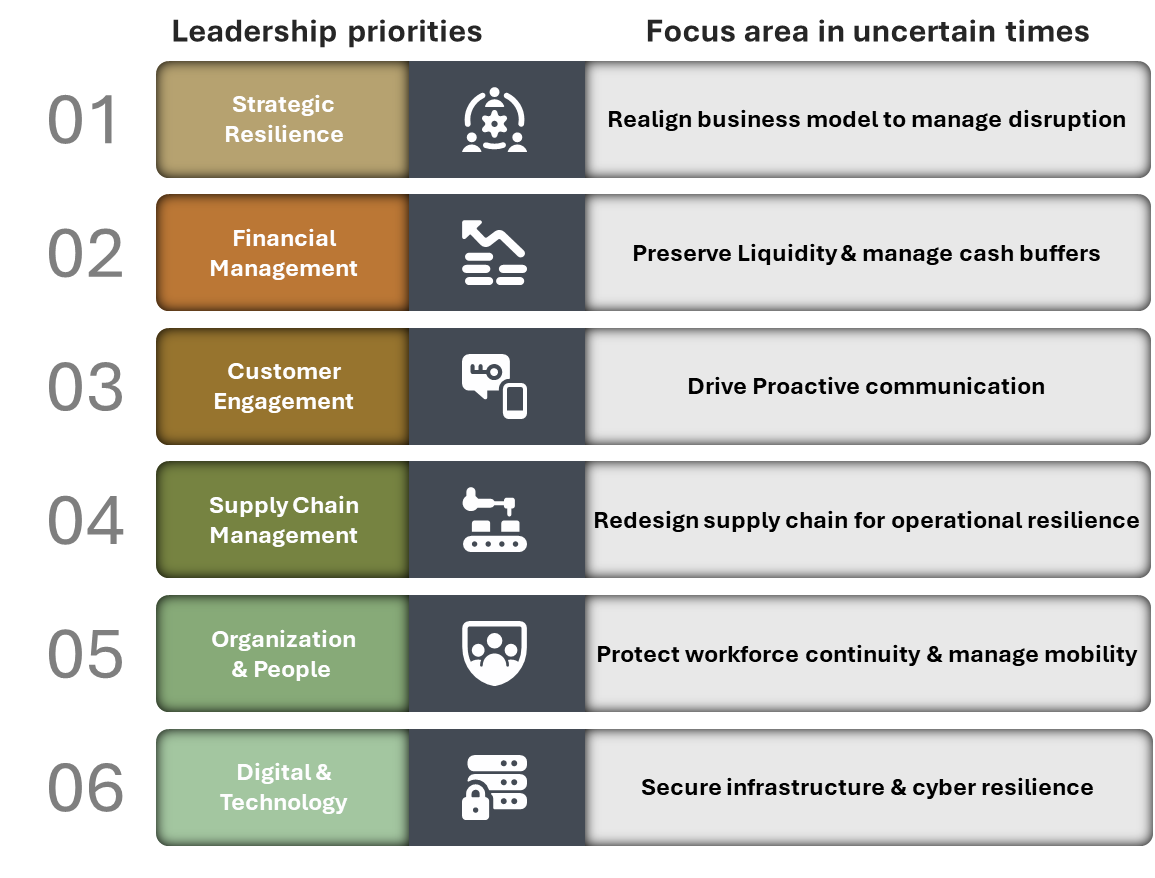

Across sectors, the impact of this disruption converges on five areas that every leadership team must address. Acting early on each one makes all the difference.

- Financial & Cashflow:

– Working capital cycles are elongating as freight, insurance and input costs reset structurally upward

– Covenant headroom is compressing quietly - weekly liquidity visibility is no longer optional

– Businesses that build a 90-day cash buffer now will have options that others simply will not - Customer & Sales:

– Discretionary spending is contracting; B2B customers are deferring long-term commitments as confidence adjusts

– Proactive engagement - clear communication, flexibility and reliability - is the most effective retention tool available

– The relationships maintained through this period will be the hardest for competitors to displace - Supply Chain & Delivery:

– Single-source dependencies are being exposed at speed - over 150 vessels remain stranded across key trade corridors

– Logistics routes optimised for efficiency must now be redesigned for resilience; rerouting is adding 30–45 days to trade cycles

– Businesses that begin supplier diversification conversations today will move faster than those waiting for clarity - People & Organisation:

– People continuity across several markets is emerging as a priority area for leadership attention

– Leadership teams are navigating complex decisions in a rapidly evolving environment

– Clear decision rights and strong internal communication are the difference between friction and momentum - Digital & Technology:

– Digital infrastructure has become a front-line operational vulnerability few continuity plans anticipated

– Sanctions monitoring, ESG obligations and cyber threats are rising precisely when management bandwidth is most stretched

– Structured governance in both areas is not a back-office priority - it is a leadership one

CHARTING THE COURSE: TEN PRIORITIES FOR LEADERSHIP TEAMS

As the strategic clock begins to tick, the imperative is preparation, not reaction. Every day of delay is a day of optionality lost. These ten priorities are not a checklist - they are the architecture of a resilient enterprise.

- Move to weekly cash and liquidity visibility, build a 90-day buffer and know your financing headroom ahead of any lender review.

- Reprioritise and defend your capital allocation - defer discretionary capex and protect the core capabilities that drive recovery.

- Stay strategically close to your customers - proactive, transparent engagement is revenue protection and the strongest defence against displacement.

- Identify the opportunities this moment is creating - new trade routes, supplier relationships and talent are available for leaders looking forward.

- Audit your supply chain from Tier 1 to Tier 3 - identify single points of failure and begin diversification conversations immediately.

- Stress-test your strategy across three scenarios - short, medium and extended - and know which initiatives to accelerate, pause or exit.

- Protect your people and your talent pipeline - communicate proactively, address expatriate concerns early & keep high-performers anchored with clarity.

- Activate rapid-response governance model with clear decision protocols, defined accountability & real-time dashboards that translate market signals into action.

- Simplify governance and sharpen decision rights - reduce structural complexity & align performance frameworks to demands of the new environment.

- Turn compliance into a competitive lever - monitor sanctions, screen counterparties & strengthen cyber resilience before potential vulnerabilities surface.

The Middle East has built extraordinary economic foundations – diversified economies, sovereign-backed institutions, infrastructure of global scale and a business community with deep experience of navigating complex environments. The current landscape tests those foundations. But it does not define the ceiling.

Disruptions do not destroy opportunity – they redistribute it. The enterprises that combine disciplined planning today with strategic boldness through recovery will emerge holding market positions and organisational capabilities that their competitors will spend years trying to replicate. Leaders who hold the wheel to steer with purpose and clarity, navigate their organisations & people to calmer waters.