Recent geopolitical developments across the Middle East have brought into sharper focus a combination of risks that extend beyond traditional financial metrics. Beyond market volatility and liquidity considerations, banks are managing increased exposure across digital infrastructure, third-party dependencies and operational continuity. These risks do not always surface on standard dashboards, but they can directly affect a bank’s ability to deliver uninterrupted services.

As geopolitical developments reshape the operating environment, the impact on banking technology is immediate and multi-dimensional. Payment systems, digital channels and customer access points are often the first areas where stress becomes visible. Institutions that maintain continuity in such conditions are typically those that have pre-defined response frameworks, clear governance and tested resilience mechanisms already in place.

In the Middle East, where cross-border flows, trade corridors and real-time payment expectations are central to banking operations, the resilience of technology infrastructure is increasingly linked to overall business continuity. This environment requires technology leaders to move beyond reactive measures and focus on preparedness, visibility and coordinated response.

A SHIFTING OPERATING ENVIRONMENT

The current environment across the Middle East reflects a convergence of multiple risk factors interacting at the same time. Elevated cyber activity, pressure on physical infrastructure, supply chain disruptions and evolving regulatory expectations are no longer unfolding separately. Together, they are making stable banking operations more complex to maintain.

What distinguishes the present environment is not the existence of these risks, but the speed and overlap with which they are emerging. Coordinated threat activity has also increased, with financial institutions continuing to remain a key target. The impact is further amplified by dependencies across digital infrastructure and third-party ecosystems, where even localized disruption can create wider knock-on effects.

For banking technology teams, this shifts the challenge from managing isolated incidents to managing a more interconnected operating condition. Understanding system interdependencies, identifying operational vulnerabilities and responding quickly across functions are becoming essential capabilities, particularly in a region where cross-border financial flows and real-time services are central to day-to-day banking.

This convergence is not theoretical — it is already visible across core banking infrastructure and customer-facing functions.

WHERE BANKING TECHNOLOGY IS BEING TESTED

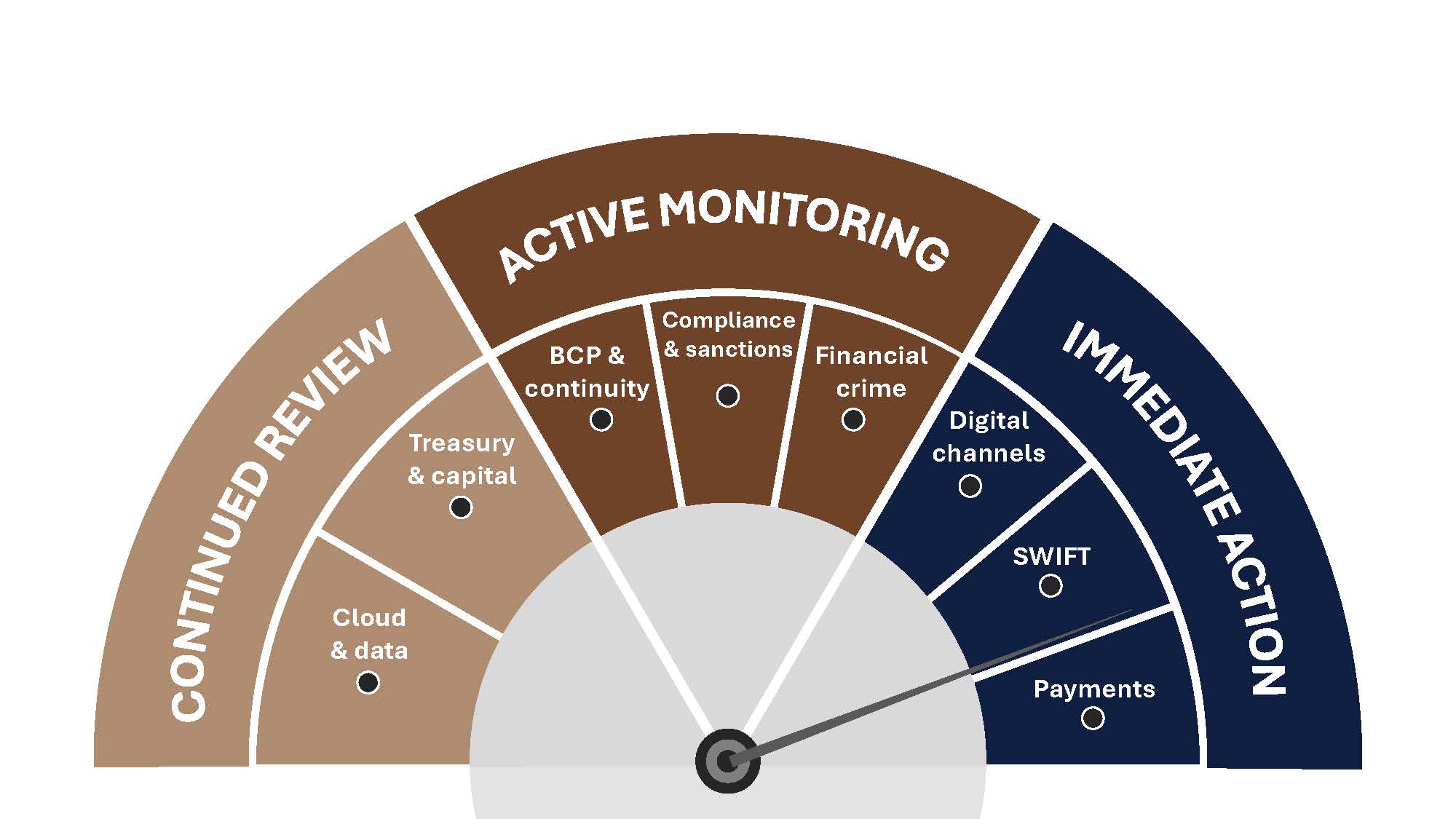

The current environment is placing pressure across the full spectrum of banking technology, from the infrastructure that moves money to the functions that serve and protect customers. The impact is not uniform — it is playing out differently across infrastructure layers and business-facing functions, with each carrying its own timeline, consequence and demand on leadership attention.

Data source: Cedar Research

Data source: Cedar Research

- Payments and Transaction Infrastructure: Payments are the most visible measure of whether a bank is truly operational. Cross-border payment timelines are extending, remittance corridors are under strain and FX settlement is becoming increasingly complex to execute reliably.

- Correspondent Banking and SWIFT Connectivity: International connectivity that operated invisibly in stable conditions becomes a priority the moment it is under strain. Correspondent relationships in certain corridors are being reviewed with greater caution and interbank routing requires active monitoring with clear contingency protocols.

- Data and Cloud Infrastructure: The assumption that cloud hosting provides inherent insulation from disruption has been tested and found incomplete. Vendor dependencies that were never formally mapped are now carrying direct operational consequence and require immediate attention.

- Capital Markets and Treasury Technology: Treasury desks are managing multiple pressures simultaneously. Trade finance platforms and treasury management systems require real-time visibility and tested contingency protocols to remain operational under concurrent demand.

- Digital Channels and Customer Service: When customers seek reassurance, digital channels are where they look first. Availability in this moment is institutional credibility. Platform stability, service desk capacity and customer communication infrastructure all require active review and clear ownership.

- Financial Crime and Fraud Management: Periods of uncertainty create conditions where customers and staff are more susceptible to deception. Fraud attempts rise measurably during elevated-uncertainty periods and rule sets calibrated for normal conditions need immediate review.

- Compliance, Sanctions and Regulatory Obligations: Regulatory expectations do not ease when operating conditions become more demanding. Sanctions lists are updating with greater frequency and compliance technology must be agile enough to absorb rapid configuration changes without delay.

- Operational Continuity and BCP: Most continuity frameworks were designed for one disruption at a time. The current environment rarely obliges. BCP and DR frameworks need stress-testing against simultaneous operational demands, not the sequential scenarios most institutions have planned for.

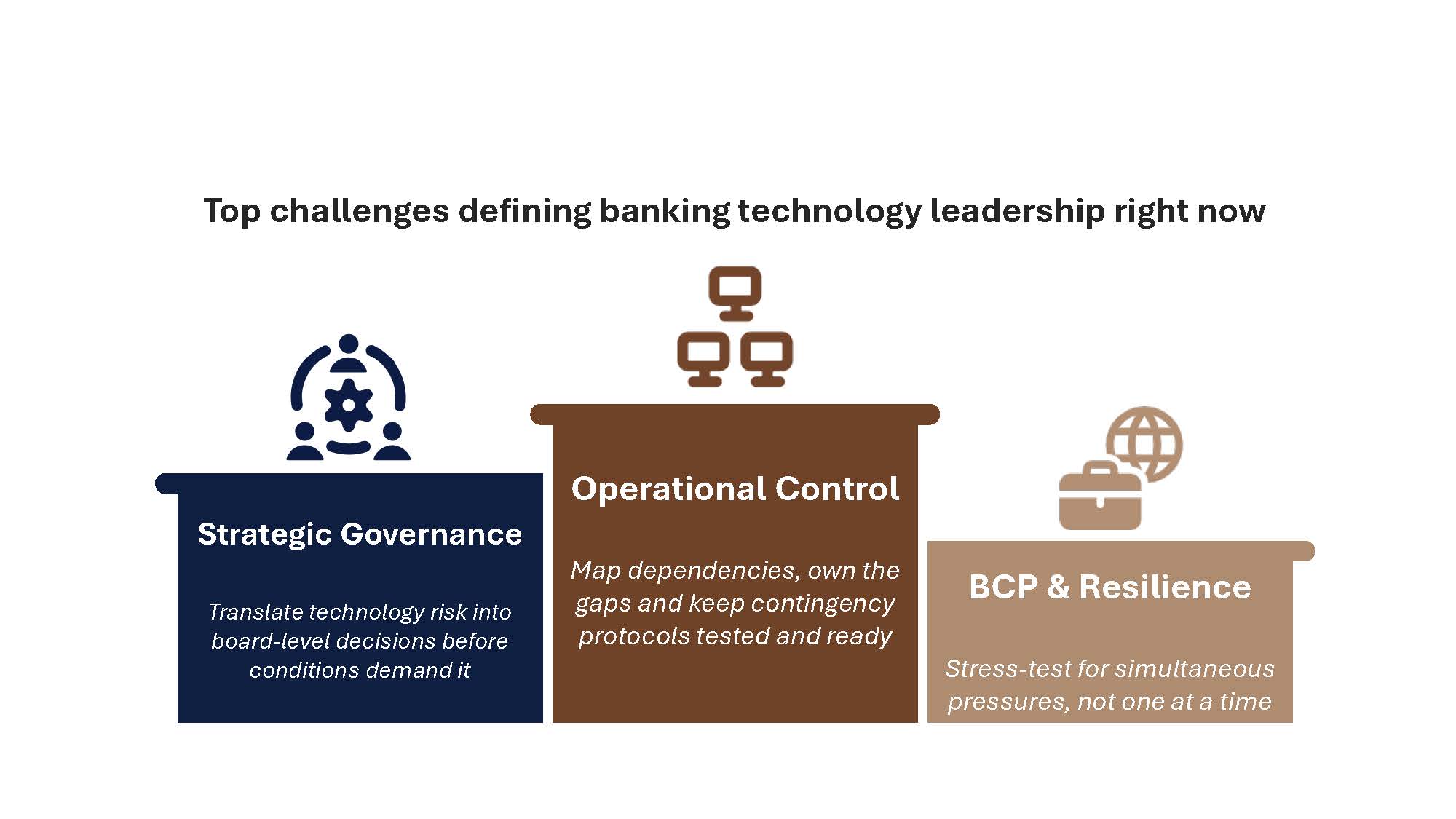

WHERE BANKING TECHNOLOGY LEADERS MUST FOCUS NOW

The institutions that emerge from periods of uncertainty in the strongest position are those that act with clarity before conditions demand it. These priorities define how technology teams can move from reactive response to structured readiness.

- Align Leadership on Technology Risk Technology risk at this moment is a governance conversation. Leadership needs structured, scenario-based briefings that translate technical exposure into clear business consequence and decision-ready options.

- Strengthen Business Continuity and Disaster Recovery readiness Most Business Continuity and Disaster Recovery frameworks were built around isolated disruption events. In the current environment, banks need to test whether these frameworks can hold under concurrent pressure across cyber, vendor, workforce, and operational fronts.

- Review Every Vendor Dependency Single points of failure often sit beyond the vendor list. Banks need a clear view of dependencies across external providers as well as mission-critical systems supporting payments, digital channels, compliance, and core operations, with mitigation plans that are active rather than pending.

- Secure Payment and Settlement Infrastructure Payment rails and interbank connectivity require dedicated monitoring and tightened access protocols. Contingency routing should be defined and tested ahead of any disruption.

- Strengthen Data Controls Today Validate data access controls, backup integrity and recovery protocols across critical systems. Elevated-risk environments expose gaps in data governance that stable periods routinely obscure.

- Protect Digital Channel Availability Platform availability is a trust signal. Establish real-time monitoring thresholds, clear escalation paths and proactive customer communication protocols before they are needed.

- Recalibrate Fraud Detection Rules Conditions that elevate customer anxiety also elevate fraud and social engineering attempts. Rule sets calibrated for normal operating periods need immediate review to close gaps that are not yet visible in the data.

- Accelerate Priority Technology Projects Uncertainty is not a reason to pause — it is a reason to move faster on initiatives that strengthen resilience. Teams that defer critical projects now will find themselves further behind when conditions stabilise.

- Tighten Compliance and Sanctions Technology Sanctions lists are updating with greater frequency. Compliance technology needs to absorb configuration changes accurately and without delay, with reporting infrastructure ready for increased regulatory scrutiny.

- Build Beyond the Disruption The technology decisions made now define operational strength well beyond the current environment. Institutions that invest in resilience during pressure emerge with a structural advantage their competitors will take years to close.

The current environment is not simply a test of systems, but of preparedness, coordination, and decision-making under pressure. In a region where financial flows, cross-border connectivity, and real-time expectations are integral to banking operations, technology resilience has become inseparable from business continuity. Institutions that can maintain stability across their digital infrastructure, even as conditions remain fluid, will not only protect operations but reinforce customer confidence at a critical time.

The advantage, however, will not come from responding in the moment alone. It will come from how banks use this period to strengthen their operating model — improving visibility, tightening control points, and building systems that can adapt to sustained uncertainty. The choices made now will shape how effectively institutions navigate not just the current environment, but future disruptions where speed, coordination, and resilience will define competitive strength.