Middle East banks are bracing for potential disruptions to liquidity, funding and credit flows. The real financial impact will depend on how long the current context persists. The recent conflict across the West Asia had its impact on financial markets, and has made every bank in the region ask the question: what does it mean for us?

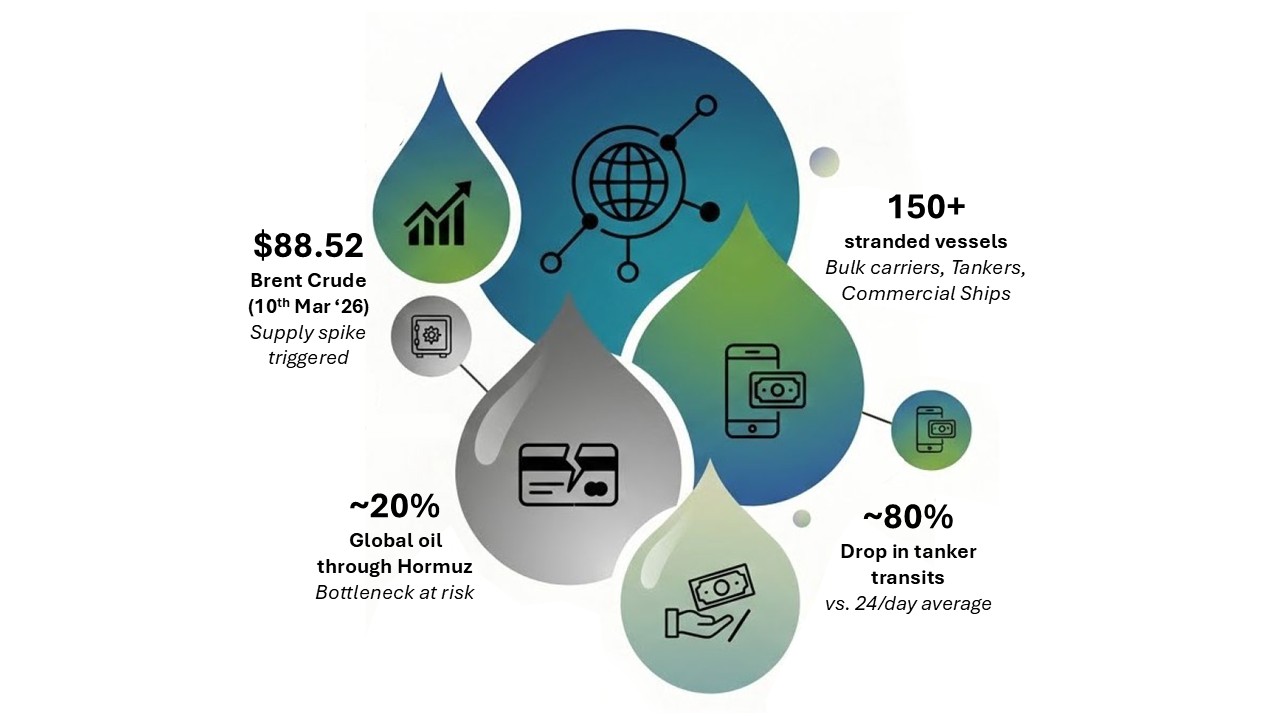

Within 72 hours of the escalation, energy corridors were disrupted, trade routes were in flux and the region’s financial system was navigating its complex period of uncertainty since Russia & Ukraine conflict in 2022.

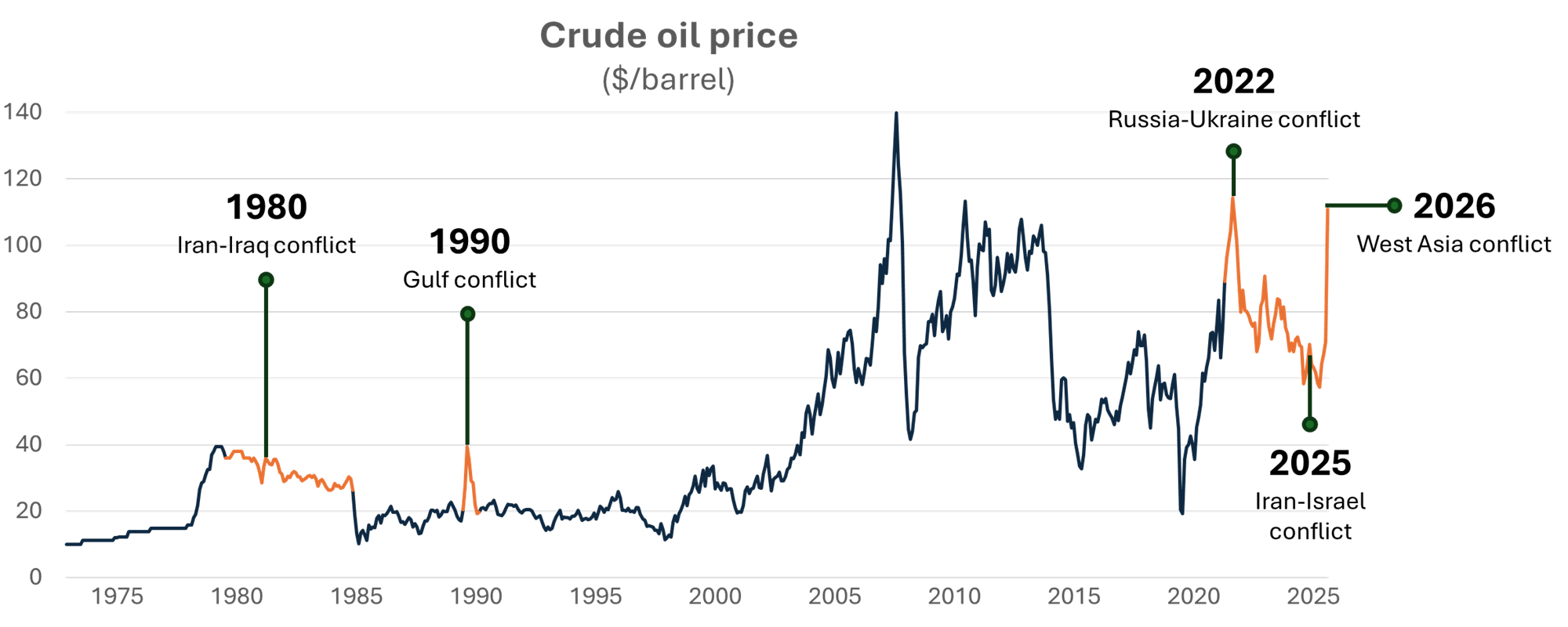

LESSONS FROM HISTORICAL PARALLEL CRISIS

Data source: Trade Economics

Data source: Trade Economics

The past is not a perfect mirror but it is the most reliable guide available. To understand where this conflict leads, it is worth examining where similar ones had ended.

The 1990 Gulf Conflict delivered the most acute banking stress - oil surged 89%, private sector deposits fell 15-21% and liquidity tightened rapidly. As a consequence, the impact quickly cascaded across key sectors. including shipping & trade, hospitality, food and real estate, broadening the crisis from an oil and liquidity event into a wider regional reset in supply chains. Shipping faced immediate disruption as transport economics deteriorated, commercial routes became less reliable and the movement of essential goods came under pressure. Regional rerouting resulted in port traffic doubling from 10 million to 20 million tons per year.

History offers a sobering reference point on supply chain risk. In 2021, the grounding of the Ever Given blocked the Suez Canal for just six days, delaying over 430 vessels, disrupting cargo worth $92.7 billion and taking up to three months for trade flows to fully normalise. That was one ship, one canal, six days. The Strait of Hormuz carries nearly 20% of global oil and LNG daily, with no alternative route. If disruption here extends into months, the baseline of resilience will shift rapidly. Sovereign rating pressure builds, funding costs rise and the banking system moves from managing a short-term liquidity challenge to navigating a structural credit event.

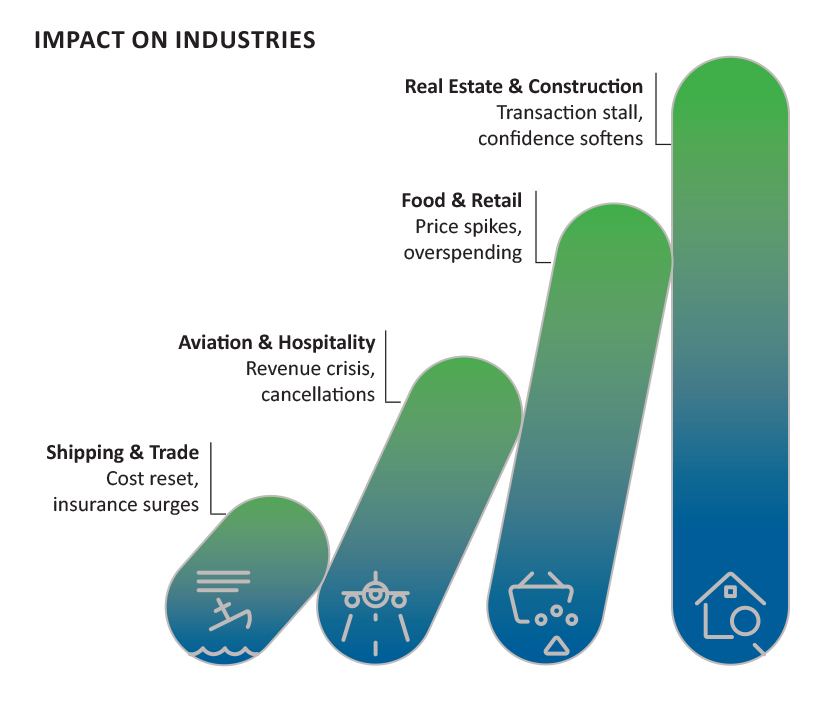

INDUSTRY IMPACT: WHAT’S CHANGING ON THE GROUND

The financial pressure is only half the story across the Gulf ’s economy, the effects are being felt on the ground.

- Shipping & Trade face a structural cost reset. Conflict-risk insurance premiums surged 5x - from 0.2% to 1% of hull value - making a single voyage on a $100 million tanker a million-dollar insurance bet. Supertanker freight rates hit $423,736 per day, a 94% spike in a single session. Supply chains for pharmaceuticals, semiconductors and food commodities are experiencing disruption - with no alternative route to replace the Strait.

- Aviation & Hospitality experienced early impact. Over 4,000 daily flights were cancelled as Gulf airspace closed simultaneously, stranding hundreds of thousands of passengers. Forward hotel bookings faced a significant decrease overnight. For a region where tourism contributes double-digit percentages of GDP, this is not a sentiment problem - it is a revenue crisis.

- Food & Retail is where the pressure becomes most visible to everyday life. With the majority of Gulf states’ food imported, supply chain disruptions are already pushing fresh produce prices higher across the region. For banks, rising household costs translate directly into consumer stress, increasing credit card reliance and accelerating retail portfolio pressure.

- Real Estate & Construction responds quickly to geopolitical uncertainty as market activity typically slows and cross-border capital flows moderate. Developers often defer new launches while buyers postpone long-term commitments such as home purchases and commercial leases. Construction timelines may also face delays due to shipping disruptions. For banks, softer property transactions reduce mortgage origination and gradually moderate collateral values supporting real estate lending portfolios.

WHERE IS THE IMMEDIATE THREAT - ASSET OR LIABILITY?

GCC banks entered this crisis from a position of structural strength - solid capital ratios, high liquidity coverage and NPLs trending downward. That foundation matters. But capital buffers are defensive; they absorb pressure, they do not prevent them from forming.

The crisis strikes both sides of the balance sheet at once - and that simultaneity is what makes it challenging.

On the asset side, the pressure is real but lagged. Trade finance and working capital facilities are the first to feel it, as port disruptions and insurance withdrawal stretch SME cash cycles. Aviation, hospitality and trade-linked corporates face covenant stress within 60–90 days. Yet these signals take weeks to appear in formal credit classifications - the clock is running invisibly.

On the liability side, the threat is immediate and behavioural. GCC banking systems carry a structurally mobile deposit base - expatriate-heavy workforces, internationally mobile HNW clients and corporates with offshore optionality. Wholesale spreads may widen if international banks pull back from the region, compressing capital market access precisely when it is most needed.

“The asset side impact will be driven by the supply chain and cash cycle uncertainties. Impact on liabilities influenced by expatriate customer base.”

SEGMENT-LEVEL BANKING STRESS SIGNALS

The crisis does not hit every banking segment with the same velocity. Stress emerges in depending on their exposure to trade disruption, consumer sentiment, liquidity conditions and borrower mobility. More structurally, insurance costs across industries are being reset upward - not as a temporary conflict premium, but as a permanent recalibration of regional risk. That cost increase will outlast the conflict itself.

- SME Banking: These are the first in line to be impacted by the crisis. SMEs in the region are primarily traders dependent on port access. With the reroute around the Cape of Good Hope, 30-day working capital cycles have elongated to 60-90+ days. Cash flows are on hold, making daily delinquency monitoring an absolute necessity.

- Corporate Banking: Stress is sharply tiered. Energy firms and governmentlinked enterprises remain largely contained, with infrastructure contracts expected to re-accelerate within 3–6 months as fiscal stimulus kicks in. The immediate risk sits with trade corridor-dependent borrowers facing a dual P&L squeeze - fee income and provisioning costs moving adversely, simultaneously.

- Wealth Management: The $83 billion in FDI that flowed into Dubai and Abu Dhabi over the last decade is now sensitive to “hub risk.” While regional players are staying put, international HNWIs are already tactical de-risking, moving from regional equities into USD cash and Gold ETFs.

- Retail Banking: Retail behaviour typically follows a “spurt and slump” cycle during uncertainty.

– Card Spend: Residents front-load essentials and fuel purchases, briefly spiking transactions. This early surge is misleading; spending quickly plateaus while delinquencies begin quietly building underneath.

– Auto Loans & Mortgages: Applications are down 20-40% as buyers defer big-ticket commitments. For mortgages, departing residents deflate collateral values simultaneously, converting performing loans into structural exposure before a single default is formally recorded.

– Collections & Recovery: When borrowers exit the jurisdiction before meeting obligations, recovery becomes structurally difficult. Unsecured personal loans carry the highest exposure, but the risk cuts across cards and mortgages equally. - Treasury & Capital Markets: Face a three-way squeeze. Wholesale funding spreads are widening and equity capital pipelines are tightening. Treasury desks must manage bond portfolio losses as yields rise, defend FX positions against dollar strength and roll short-dated funding obligations -> all simultaneously.

- Microfinance & Community Lending: The most silent pressure point. Small traders and informal-sector expatriate borrowers have no buffer against supply chain disruption. Repayment capacity tested within weeks; cross-border enforcement is virtually non-existent. This segment surfaces in NPA data first and earliest.

- Digital Infrastructure emerged as an unexpected pressure point. Infrastructure disruption to data centre facilities across the region degraded over 100 cloud services simultaneously, taking several commercial banks’ mobile banking platforms and payments infrastructure temporarily offline. For the banking sector, this introduced a new category of operational risk - one that no business continuity playbook had fully anticipated.

REGIONAL CONNECTION: A RIPPLE EFFECT

The pressure is not contained to the Gulf. For regional players like India, the impact arrives through a different channel - as a significant importer of Middle Eastern oil, India faces a widening trade deficit and a weakening rupee as energy prices rise. Government-owned banks with large bond portfolios face mark-tomarket losses as yields rise on inflation concerns. Industry analysts view suggest that if expatriate workers return home in meaningful numbers, the remittance and deposit flows that Indian banks rely on could soften - creating a secondary liquidity consideration in the subcontinent.

STRATEGIC PLAYBOOK: 10 KEY FOCUS AREAS

As “credit clock” begins to tick, for banks across Middle East, the immediate challenge is preparation rather than reaction - every day of delay is a day of optionality lost.

- Know your liquidity position: understand where your funding sits today and what happens if deposits shift. Pre-position buffers early.

- Build a monitoring nerve centre: dedicated teams tracking trade corridor activity, sector stress and macro signals in real time, translating into balance sheet action.

- Accelerate digital adoption with clients: onboard clients to digital payments, trade platforms and treasury services can lock in usage long after the crisis passes.

- Tighten where it matters: not everywhere. Apply tighter credit standards to the most exposed sectors and tenors. Avoid blanket retrenchment.

- Review digital resilience: infrastructure vulnerabilities have emerged as a new category of risk. Stress-test systems and back-up protocols now.

- Manage FX actively: monitor currency movements and funding cost shifts in real time. Treasury desks should be on active watch, not passive review.

- Deepen advisory and treasury partnerships: provide proactive treasury advisory become strategic partners rather than just lenders.

- Watch the early warning signals: 30–60 day delinquency trends will tell you what is coming weeks before formal classifications do. Check them daily.

- Stay close to clients: proactive, transparent communication across all segments builds confidence. Banks that go quiet lose trust faster than those that engage.

- Revisit collateral and tenors: shorter tenors and stronger collateral requirements for vulnerable segments is prudent portfolio hygiene, not overreaction.

The institutions that combine defensive discipline today with strategic boldness through the recovery will emerge with client franchises, market share and relationships that took their competitors a decade to build. After all, crises do not destroy opportunity; they redistribute it!