The winning formula for the new age is no longer just

about customer segmentation, but also about providing

world class differentiated experiences

From driving transaction efficiency to sophisticated CRM platforms, banks have invested millions of dollars in building operating models that drive superior service levels. However, the customer engagement experience is what really matters. The question that then needs to be answered is: do all customers have the same experience? Or is a distinction drawn between different segments? If so, what is the right approach to segmentation?

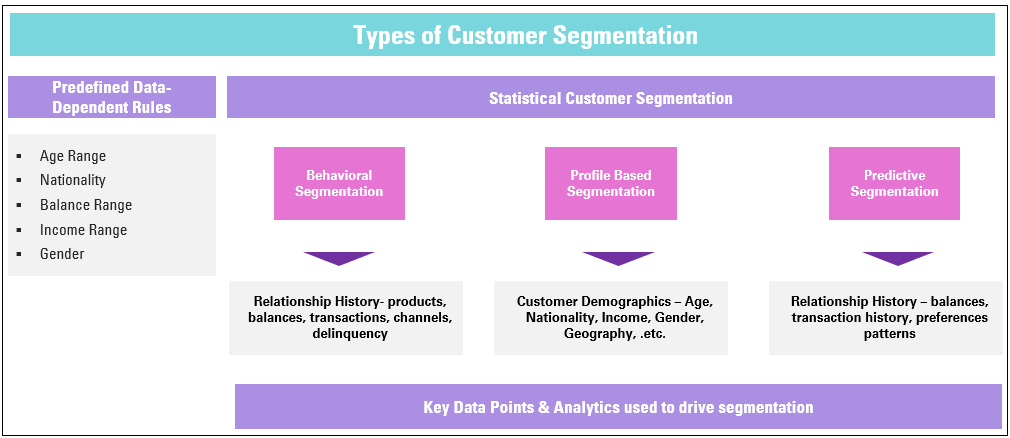

Customer segmentation is the Holy Grail for leading retail banks. And it is viewed as the greatest thing since sliced bread in the consumer and services world. Those who succeed not only get the science of differentiation right, but also ensure it is implemented effectively. This is not just theoretical KYC norms or regulatory compliance. This is about really knowing who the customer is. Not just from a demographic or sociographic standpoint – the age, income, gender, occupation, etc. all do matter. It is beyond that. It is also about knowing banking preferences and profiling customers based on transaction behaviour, and more importantly determining what matters to them.

The conventional logic of having customers defined as Mass Retail, Mass Affluent, HNI and Ultra HNI continues to form the bedrock of segmentation. These definitions are primarily driven based on the net-worth or income levels of the customer, or the relationship value that the customer holds with the bank. Banks have, however, moved further to also identify segments to focus on from a vertical classification – a classic example is Millennials, whose product, service and channel preferences are new age and quite different from traditional customers. The Merrill Edge programme, driving online investments by young people who stand to inherit large sums, is a good example of this.

While profile-based segmentation based on customer demographics remains quite heuristic, behavioural segmentation helps drive grouping and analysing customer preferences from the standpoint of product holding, balances, patterns of channels and transaction activities. And the sophistication of analytics has also brought a new perspective to the game, with micro-segmentation holding the key to customising product and service offerings to smaller groups with homogeneous interests, behaviour and preferences. Predictive segmentation helps apply previous knowledge to these micro segments within the existing customer portfolio, to address a business question that begets an answer – for instance, which of these microsegments are dissatisfied, and what approach would need to be adopted to address a particular pain-point or need for that particular micro-segment? This becomes even more pronounced when the underlying portfolio is represented by a segment that is more valuable, or whose attrition poses a higher risk.

HNI: who, why and what?

The classic industry definition of a typical HNI customer is someone with investible assets over $1 million, although this varies between geographies and banks. There are an estimated 17 million global HNI with $65 trillion in wealth. 1% of that constitutes the Ultra HNI population, typically defined to be with investible assets over $30 million, and this segment holds over 35% of the global wealth. North America and Asia Pacific geographies make up more than half of the HNI population.

The HNI segment is sought after by banks as it tends to provide a much higher stability and a framework to drive the liability strategy. The focus is on building the deposit book, the investment portfolio that drives both a cost-effective liability book, and a healthy fee income structure. An effective HNI strategy could well be the secret sauce for driving profitable growth, especially when cost of capital and access to liquidity get harder to tap into.

The question then moves to what makes the segmentation meaningful. Or, put differently, what matters more to the typical HNI customer? While managing the wealth for a HNI customer is always seen as the primary value proposition, the positioning of a bank to this customer extends beyond just deposits, investments and insurance products. The maturity of the market, the awareness of the customer and also sophistication of the bank all matter when it comes to the evolution of service offerings: from an execution only model to that of an advisory model and to a fullfledged wealth management offering with holistic services. However, all things being equal, it is the service differentiation that makes a difference.

Customer engagement is all about shifting experiences. While 75% of customers reportedly prefer their primary bank to be first choice for managing personal finances, less than 40% have a positive experience to report about their provider. The name of the game, therefore, is in shifting negative or neutral experiences to positive ones. And FinTech disruption is already creating a dent in conventional wealth management portfolios with a digital approach to setting budgets, monitoring spend, reviewing saving goals, managing investments or notifications and reminders.

Innovations in channels, both with the conventional branch as well as with the digital channels, holds a very important place in service level and experience differentiation. Driving an omnichannel integrated view and access, PFM offerings over the mobile, an intuitive IVR and a personalised contact centre experience – all of these are seen more as hygiene factors. Their absence is felt more than their presence.

The challenge of personalisation is even more pronounced when dealing with the HNI segment. An estimated $41 trillion of wealth is to be transferred from Baby Boomers to Millennials by 2025, and that makes customised experiences even more critical. A strategic approach to leveraging social media and providing corporate updates, expert advice and analysis is an interesting strategy adopted by leading players such as Credit Suisse, BNP Paribas and Deutsche Bank, while mobility and anywhere access available on tap is a core value proposition at CitiGold. Free evaluation of customer financials online by USAA and the superior online banking experience of BankAm, are pertinent examples of global FIs driving differentiation through digital.

Needless to say, banks quickly embracing new rules have a head-start, not only with new entrants to the HNI club, but also existing ones who see the merits of convenience. Defining the right segment is key, as is knowing the customer’s preferences. However, predicting changing needs and aligning offerings accordingly are hugely important elements in the new age of banking. After all, it’s the most responsive to change that survive, not necessarily the strongest or, for that matter, the largest.

To read more such insights from our leaders, subscribe to Cedar FinTech Monthly View