A future-proof digital core banking system is essential to speed up innovation, meet changing customer needs and swiftly respond to the changing environment

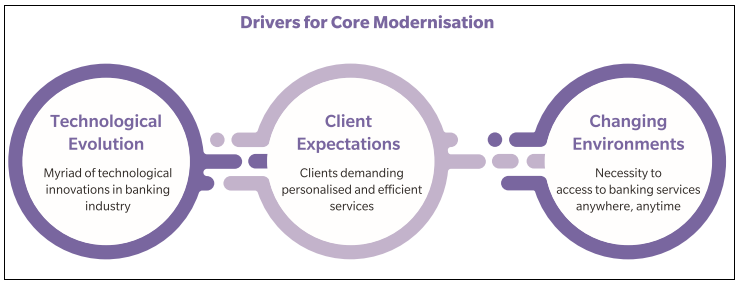

Traditional core banking no longer provides the required customer experience to acquire, retain and grow customers. Many banks are behind in making the critical end-to-end digital banking transformation due to a variety of legacy systems and fragmented data. Banking institutions must now establish a more holistic customer experience approach and digital transformation strategy- referred to as 'Digital Core Banking'. Core banking modernisation is driven by higher client expectations, changing environments, and technological evolution.

Clients are increasingly demanding services that are personalised and efficient. They want access to services and solutions digitally, using the devices they prefer, within the time frames they want. Therefore, the focus should be on front to end digital transformation and enabling seamless customer-centric servicing that delivers the right interaction at the right time via the right channel.

There is a fair chance banks have already adopted a fancy app and website with features such as chatbot or Al, but true digital transformation cannot happen just at the channels as often the core technology is too rigid and too slow to support customer needs. Banks have started to understand that digital transformation can only happen when digitisation is used throughout a bank. To become truly digital, banks should also invest in replacing the core universe to meet higher client expectations and adapt more quickly to changing environments some of which may not be presently known.

A core banking system designed and build on digital principles can mean the difference between success and failure for most banks. Regardless of the size and region, banks should be able to address the increasingly demanding needs of customers and regulators, operate as efficiently and cost effectively as possible and launch new products in no time.

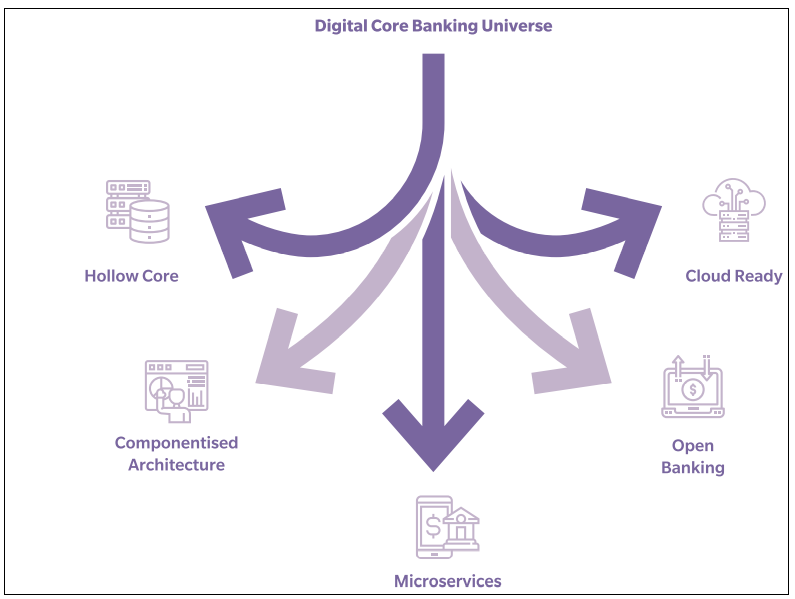

Core Banking in the Digital Age

The Digital Core Banking universe which a bank should focus on to fully transform from legacy core to a core banking system for the digital age consists of the following key principles: Hollow the Core, Componentised Architecture, Microservices, Open Banking and Cloud Readiness

Hollow the Core

The complex monolithic core is expensive and rigid. Expensive due to outdated technology where it is difficult to find the skilled resources to maintain the monolithic core and rigid as it is unable to quickly adapt to new requirements due to changing customer or regulatory needs. The primary purpose behind this concept to "hollow the core' is to have core banking platforms solely act as systems of records or posting ledgers.

New capabilities or customisations specific to bank or region should be build outside the core. The mantra for new core is literally zero customisations, ensuring standard offering of the product explained or demonstrated to business.

The approach to hollow out the core or abstract the domain capabilities from the product processors offers greater flexibility and innovation and enables IT teams to setup the platforms for a modern ready-to-use design powered by the latest best in class technological solutions.

Componentised Architecture

A Digital Core Banking system is structured as a modular and componentised platform of retail and corporate banking, with options to choose products aligned to customer segments, and business priorities. A componentised architecture provides flexibility for the bank to decide what to deploy, and when to deploy or upgrade a component.

The next generation banking solution offers discrete and smaller components with eventual flexibility. Componentised modules extend real-time digital processing capabilities and the potential of banking modernisation opportunities while continuing to feature the core banking product innovation, processing ability, security, performance, and reliability.

Component-based architecture incorporates standalone configurable components instead of functionality usually embedded in channel applications across the business. This approach allows banks to protect existing IT investments, releasing capital for innovation and enhancements that attract and retain customers of the bank. A component-based approach to core modernisation is to facilitate customer-focused, agile business processes; to renovate product and servicing offerings and related pricing.

Microservices

The banking software industry has reached another milestone with the roll out of functionally rich microservices-based architecture to strategically transform core banking systems at scale and revolutionise banking. Unlike legacy monolithic core banking systems, microservices are independently deployable functional APIs which are cloud-native and cloud-agnostic with tangible benefits.

Core banking microservices can be deployed autonomously in the enterprise along with the existing systems if such existing systems still serve the purpose. Microservices enable banks to offer an agile, services-based architecture for other banking applications and digital customer journeys.

A microservices strategy offers banks the benefit of independent component upgrades, with zero down time and minimum impact on 'business as usual', allowing banks to significantly reduce total cost of ownership for their existing core banking platform and quickly react to market opportunities, such as building extensive set of standalone microservices services for Payments, Dedupe, Fraud Management, Account and Deposits, Lending, Product Catalogue, Pricing and Analytics.

Cloud Ready

Cloud ready core banking platforms are relatively new but are set to become more mainstream. A cloud platform is the solution to numerous core banking challenges, like high IT infrastructure cost, frequent hardware upgrades, round the clock availability, latest security levels, and scalability. However, the banking industry still shows reluctance to adopt cloud-based solutions due to potential security concerns over data leaks. On the contrary, the latest cloud-based solutions offer security standards that surpass on-premises solutions.

A cloud-based platform empowers you to spend more effort and money on the areas where you can create a 'wow' experience for your customers instead of focusing on IT, security, and operational issues. Industry trends prove successful implementation of pure cloud-based core banking platforms by both traditional and digital only banks. In fact, we can surely say that the adoption of the cloud will be a critical factor in clearly differentiating leaders from laggards. Leader banks will emerge as early adopters providing smooth digital experiences to their customers with lagging banks unable to stand up to their competitors in this new age of digital core banking.

Migrating core banking systems to the cloud presents banks a limited opportunity to achieve contradictory objectives in a single move: reducing costs while enhancing scalability and flexibility.Cloud-based banking enables you to automate business processes and reduce process turnaround time. Interlinked software and hardware components should be designed to maximise the offering of the Cloud. This results in reduced cost and increased operational efficiency. You can optimise your focus to understand customer needs and serve your customers better, rather than maintenance of outdated technology or managing complex integrations with legacy systems.It has become clear that any banks relying on legacy architecture and legacy systems cannot compete against more innovative digital competitors. With the right cloud platform, the bank is ready to serve customers and rapidly respond to new products and services. We believe the time has come to move core banking processing to the cloud, and it should be in the minds of all architects and banking executives.

Open Banking

Open APIs serve as a bridge between core banking components to connect banks with the FinTech ecosystem In providing Improved customer service, end-to-end straight-through processing and assist banks in reducing their dependence on legacy systems in lieu of lightweight architectures built on microservices and the cloud. The banks ignored Fintech competition for quite some time, hoping it would go away.

The Payment Services Directive 2 (PSD2) has required banks to release customer data in a secure, standardised form, to be shared among authorised organisations online. This part of open banking makes it possible to pass customer information to third parties, who can use this data to create new products. It is a way of enabling customer data sharing - if they give their consent - to enhance competition between the banks.

Thanks to this open banking framework and standards, a huge amount of transactions in the future will flow through channels owned not by banks but by FinTech and third-party technology firms in the new enterprise ecosystem. Customer experience is a top priority and it is likely that, with the forthcoming exponential growth in transactions through digitisation, banks might struggle to sustain or compete on legacy systems. Open banking presents a unique opportunity for challengers where customers can easily switch banks to take benefit of better products and lower fees. This will lead to opening competition between banks, FinTechs and other services providers, allowing customers to easily switch between providers.

Conclusion

Legacy core banking systems have been constantly modified to deal with changes in business practices, resulting in this legacy becoming more complicated to manage. Banks must explore the Digital Core Banking universe meticulously to modernise their core banking systems. The journey to core modernisation will take time and those planning to start in this year should expect the incremental digital core universe to be fully realised in 3 to 4 years. The typical model allows 6 to 12 months for planning, preparation, and pilot programs, and 2 to 3 years for implementation.

To read more such insights from our leaders, subscribe to Cedar FinTech Monthly View