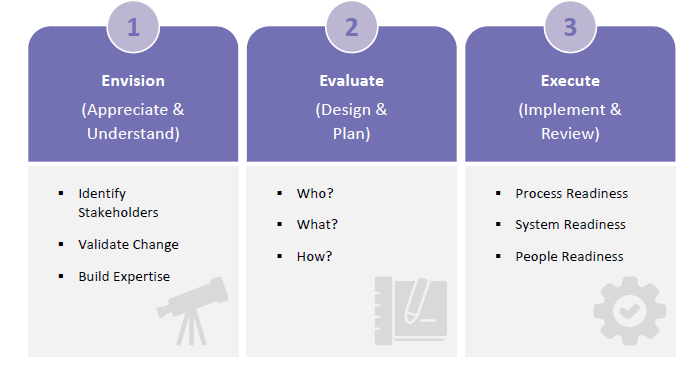

In the current scenario, regulatory reforms are considered a phase of managing change from a financial institution’s perspective. Reactive or proactive, adapting to global banking regulations are imperatives for banks. During this phase of change management, financial institutions must consider the 3Es – Envision, Evaluate and Execute

The Covid-19 pandemic has indeed had an impact on the way banking is done globally. From customer onboarding to customer servicing, there has been a significant amount of digitalisation incorporated. On a positive note, financial institutions are welcoming these changes as it is leading to the optimisation of banks’ efforts. On another note, regulatory authorities have shifted their focus from rapid technology innovation to tightening the existing policies and guidelines focusing on risks associated with technology, data usage and operational risks. With this in consideration, the authorities are taking a combination of reactive as well as proactive measures Adapting to such global banking regulations is considered a phase of change management. It is imperative for financial institutions to view this phase of change management with the following 3Es - Envision, Evaluate and Execute:

Envision (Appreciate & Understand)

Envisioning talks about understanding the regulatory guidelines from an end-to-end standpoint. In 2019 when the regulatory authorities of Europe brought out PSD2, every country had its own interpretation of PSD2 and, in turn, developed multiple standards. This led to global financial institutions implementing multiple such standards resulting in cost escalations. Hence, envisioning the regulatory reforms includes the following 3-step approach:

Identify stakeholders: Typically, the guidelines for banking regulations are released by the regulatory authorities well in advance for banks to have an end-to-end understanding and appreciation of the upcoming changes. Hence, it is also important to highlight that it is at this stage that the key stakeholders involved are to be identified and brought together from multiple banking functions, including business, audit, risk, and compliance.

Validate the change: To avoid misinterpretation, banks need to validate the guidelines. Further, this could be performed in multiple steps: the validation could happen directly with the regulatory authorities based on their accessibility. It could also be done by building consortiums with peer banks and involving third-party experts. Banks typically go for a combination of approaches. It is also important for the banks to envision a high-level analysis to understand the impacted areas.

Build expertise: Some of these global banking regulations could be very new to the industry, and some could be enhancements to existing guidelines. Building expertise in the required areas forms a strong foundation for the next stage of design and planning. However, it is not always necessary to build expertise in-house. It could be through third-party providers or an appropriate combination of in-house and external experts.

Often while the banks focus on envisioning the adaptation to banking regulation, the aspect of documentation/building know-how is left behind. Banks must remember throughout the journey that it can only be process-oriented rather than people dependent.

Evaluate (Design & Plan)

Evaluation, i.e., design and planning, is a key phase for the financial institution, forming the blueprint. Further, it is this phase that involves the facilitation of any applicable decision making by the leadership team. The evaluation phase typically answers the following questions:

Who?

- Who are the stakeholders from the bank involved, including

decision-makers? - Who are the external stakeholders involved? Is there are any

third-party assistance required?

What?

- What is the objective/purpose of the change and the allocated

timeline? - What are the impacted areas to be focused on and respective

budget allocation?

How?

- How is the change being implemented?

- How is the change management being managed, including the

governance?

The outcome from the evaluation phase forms the foundation from not just the execution perspective. It also offers an outlook on the institutionalisation of the process for the bank post the changes.

Execute (Implement & Review)

The execution or the implementation phase may be viewed with a 3-step approach.

Process Readiness: Ensuring the process is aligned to the new regulatory changes and the system is critical. It is important to reiterate at this point that a change management initiative is considered successful only when the dependency on people is removed and all the focus is on the redefining and institutionalisation of processes. In large scale implementation, this could take an angle of business process reengineering. In some of the small to mid-size implementations, it could take the angle of business process optimisation. As a direct impact of the pandemic, banks are focusing on the digitalisation of their internal process. This means they optimise the turn-around times, cost involved, building intelligence into processes to minimise human intervention. Hence, consideration of intelligent automation could prove to be worth it in the long run. However, it requires careful evaluation of feasibility and returns on investment.

Systems Readiness: Catering to changes to the system usually involving assistance from the solution providers. Considering the impact analysis performed in the previous stages, one or more systems/applications could be impacted. This could involve typical cycles of requirements gathering, system installation, testing and data migration, stress, and vulnerability testing. Banks need to traverse through the journey, ensuring each milestone is completed with utmost quality assurance.

People Readiness: Often, people readiness is an area that gets deprioritised. The factor of people readiness has a long-term impact on the change being brought into the system. People readiness is not just important from an execution perspective but also a postimplementation perspective. People must be trained well and certified on the new system, enabled with the processes to ensure that day-today activities are carried out seamlessly. The execution phase is crucial from an implementation standpoint, and documentation of key learning and continuous review of the change implemented. During continuous review, banks will have a perspective on factors such as return on investment and further enhancements that might be required for running the bank and changing the bank.

To read more such insights from our leaders, subscribe to Cedar FinTech Monthly View