Driving Enterprise & Individual performance with a balanced scorecard

The SelectIon of

Measures is Important

To drive Individual Performance.

DRIVING ENTERPRISE PERFORMANCE

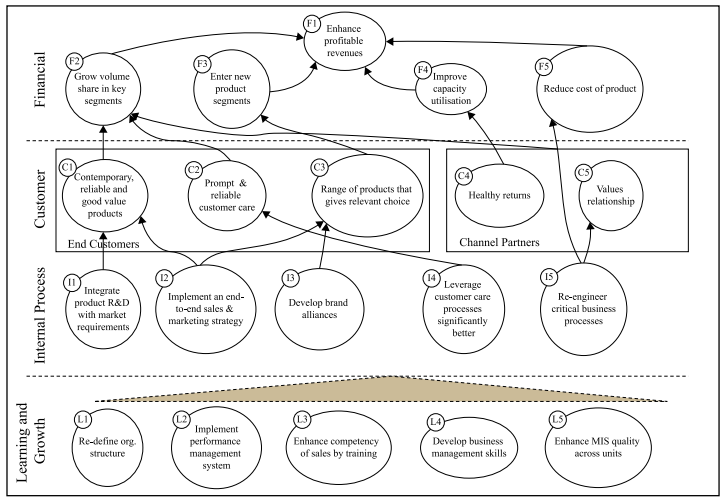

Illustrative Balanced Scorecard Strategy Map

Organizations are keen on becoming strategy-focused, and drive enterprise and individual performance. Management often asks HR to formulate key performance indicators (KPIs) that could drive individual performance. However, before developing such individual performance measures (IPMs), it is critical to develop an enterprise performance management (EPM) system so that the IPMs are aligned with the strategy. The most widely used EPM tool in the world is the balanced scorecard (BSC).

How does the balanced scorecard work? It is critical to first identify the top 20- 25 financial customer processes, and organizational and IT objectives that the firm wants to focus on. A dashboard offers a cockpit view of the strategy. Organizations often lack focus in executing the strategy. This compels them to prioritize and identify the most important financial and nonfinancial objectives they need to deliver on. Then comes the critical aspect of measurement, i.e., identifying performance measures to determine success in delivering the strategy.

Measures can be “lead” or “lag.” Most financial measures are lag. You only know how well you have done after the event is over. For example, quarterly earnings are a lag measure; in other words, they cannot be fixed once the quarter is over. It is, therefore, important to create lead measures. A good example is the frequency of customer meetings. The assumption is that the more the meetings, the higher the likelihood that the organization will meet its financial targets. The selection of measures is important to drive individual performance. If the sales team is in a position to meet its targets by selling more to existing customers, then the measurement and target of sales to existing customers becomes critical. However, do not attempt to institute too many measures. Around 25–30 measures shall suffice.

OWNERSHIP AS TARGETS

Just as one needs to have examination grades, there is a need to set targets for the measures selected. Many organizations either set too many aggressive targets that stretch the limits of organizational capacity, or do not have or allocate enough resources to deliver the targets. Often, I have found that setting 4–6 aggressive targets is enough to implement the strategy. If you focus and push hard enough on these targets, you are likely to achieve the desired results. Also, remember to have some easy targets as well. For example, in times of organizational transformation, one is not likely to get high employee satisfaction.

Identifying owners for the key strategic objectives is a critical step in focusing enterprise performance at the executive committee level. Key members of the executive committee need to take ownership of effectively implementing the strategy. Often, these areas will be within their operational control, and they will be responsible for them in any case. Moreover, they may be asked to look after objectives that may not be under their operational control, but are still important for the organization. Lastly, inventory the projects running in the organization and align them with the strategic objectives. The purpose behind investing in projects is to effectively execute the strategy. Projects that lack the capability of driving enterprise performance are questionable and could be dropped.

I would like to re-emphasize that unless there is clarity on enterprise direction, creating aligned individual performance measures will be difficult. Remember not to incentivize for delivering the wrong objectives. Otherwise, the strategy will remain where it normally gets stuck – as another confidential document on an executive’s shelf!

DRIVING INDIVIDUAL PERFORMANCE

Remember the Tom Cruise movie, where he’s a sports agent, and the guy he’s representing reminds him what’s important. In high-growth markets, finding good resources is difficult, and cutting a fixed paycheck isn’t enough anymore. This looks like you have to turn into Tom Cruise (not a bad option!), and learn how to respond to employees’ expectations nowadays. They may not be as vocal as Tom’s client, but the thoughts are the same. Loud and clear—show me the money!

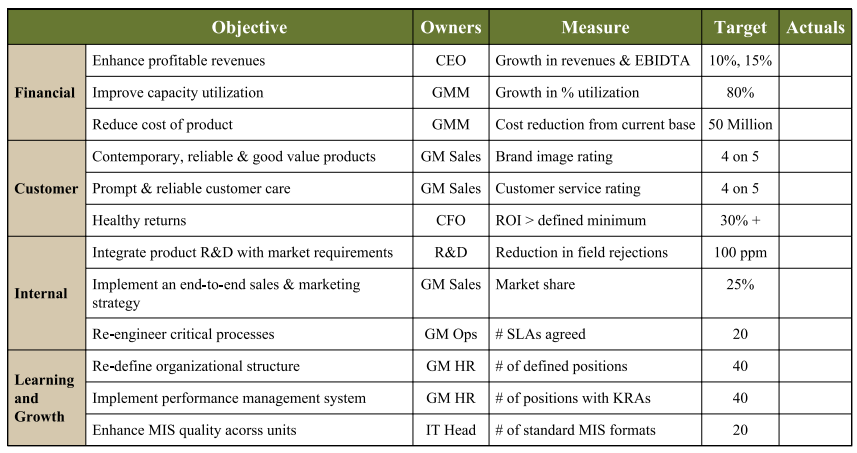

Balanced Scorecard Abridged Snapshot

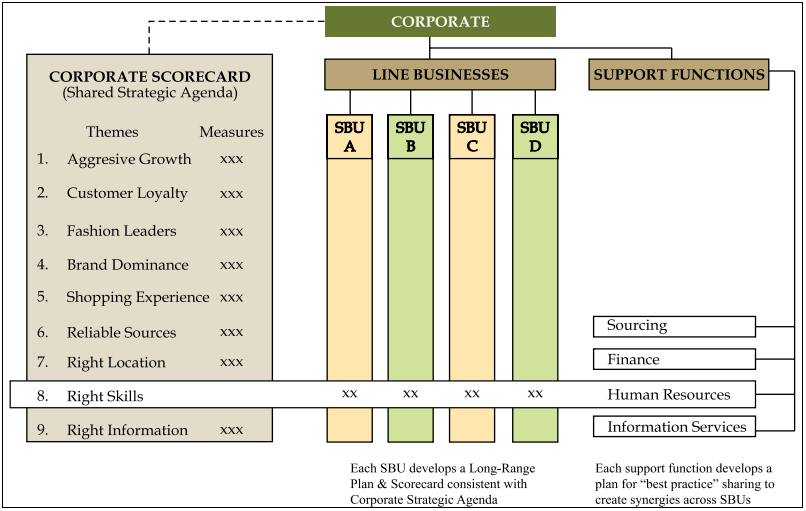

Cross Business Synergies

It is therefore essential to add a strong annual component of variable compensation based on the performance record of meeting specific targets. The concept is not new. For years, KPIs, KRAs, MBOs have existed. But their importance today is greater, especially with their link to compensation. Surveys indicate that employees place 60% importance on compensation, and the balance on hygiene factors. In the Middle East/Asia, the 60% can rise to 75%, so let’s get it right.

Designing good Individual Performance Measures (IPMs) starts with the issue of what to measure. As I indicated in an earlier chapter, it is important to have clarity on the way forward strategy, and if you have built an Enterprise Performance Measurement System/ Balanced Scorecard, you should be quite clear on what the top 30–40 strategic corporate objectives are. Use them as a reference framework, combined with operational responsibilities, to identify key measures of individual performance. Remember the most important factor here is that you must measure an individual’s performance on factors directly under his/her control. Often, I’ve seen corporate profit as the primary criterion for measuring the performance of employees. That is too generic and a person’s performance often cannot directly relate to profit or drive it. So, it is better to have a measure specific to a person’s area of responsibility.

Identifying owners for the key strategic objectives is a critical step in focusing enterprise performance at the executive committee level.

How many measures does one need? No more than 4–6. I have seen companies trying to measure employees on 15–20 measures. This approach never works. When a firm finds it hard to meet four different targets consistently, how can one expect an employee to do so? Also, HR should evenly divide the measures between the perspectives: customer, financial, process, organizational, and IT.

The next issue is the relative importance, or weightage, of the measures in terms of the organization's strategy and goals and the person’s role. So, if increasing profits is the key to the organization's business, I would not hesitate to put 35% weightage on that, on the CEO ’s IPMs. If maximising sales to existing customers is the key, then on this measure, the same logic would apply.

Setting targets on these measures becomes an issue. There is always a tendency to play with the target number: the employee wants to make it easy to achieve, and the employer, more difficult. I can only say that the best thing is to do it in an honest way. If two out of the 4–6 targets need to be challenging, make them challenging, but support the employee if he needs corporate assistance to deliver those.

My last word on this is that you should make sure that it is easy for the employee to understand all targets and objectives, and that at the end of the day you can accurately measure the inputs. And let the money at the end of the IPM rainbow be real for employees—at least 15% of fixed compensation at the junior level— going up Identify 4–6 measures • Weigh them correctly • Set targets carefully • Create a mix of difficult and easy targets • Focus on direct control factors • Pay for performance to even 200% plus for the CEO for successful performance. If you show employees the money to drive performance, meeting the same expectation from shareholders will be easy.

Sanjiv Anand, Chairman, IBS Intelligence and Cedar , is an author, management consultant and an alumni of NYU Stern and Harvard Business School. Sanjiv can be reached at SanjivA@ ibsintelligence.com